✅ Buying AI Beneficiaries and Selling One AI-disrupted Business

Staying the course during market uncertainties. Indiscriminate SaaS sell-off provide opportunities to reallocate capital.

If you are new to SWI, check out our FAQ and Owner Manual.

I am buying more shares in the most AI-beneficiary businesses, one of which is trading at ~17x FCF (>5% free cash flow yield) and with a 15-20% free cash flow CAGR over the next 5 years. That means the expected return is at least 15-20% in the next 5 years.

The proceeds will come from the sale of SPS Commerce, the least AI-insulated business in the Sleep Well Portfolio.

Before we dive in, a few smarter people have already made the call about the current SaaSocalypse:

One of whom is NVIDIA CEO Jensen Huang, he said:

‘Wall Street has got it wrong’. - Q4’2026 earning call.

He argued that it was ‘the most illogical thing in the world’ to sell enterprise software based on AI-increased demand and utility. Jensen Huang said AI will not replace software but will increase demand for platforms like ServiceNow, as agents will run on them to boost productivity.

The Trade Desk CEO, Jeff Green, echoed with a few details.

Right now, Wall Street has an unprovable bear thesis — “software is dead.” There is fear that Claude and tools like it will enable developers to duplicate Salesforce or The Trade Desk. During a time when the market can’t prove that thesis wrong, the market and the sector go down. What I think they’re missing is that the best companies in the world work hard every day looking for an edge. We’re all looking for every possible practical application of AI, new tools and every other possible advantage. AI changed a lot, but it didn’t evaporate integrations, moats, trust, customers and tools — let alone people with esoteric expertise and obsessive passion to improve things.”

But are these views applicable to our businesses?

Absolutely. They also support my findings that AI is a net positive, particularly for businesses that possess proprietary & regulated data, platform solutions, operate a mix of physical and software operations, and are actively using AI to improve operations.

Link to detail findings in this article

TLDR (too long didn’t read):

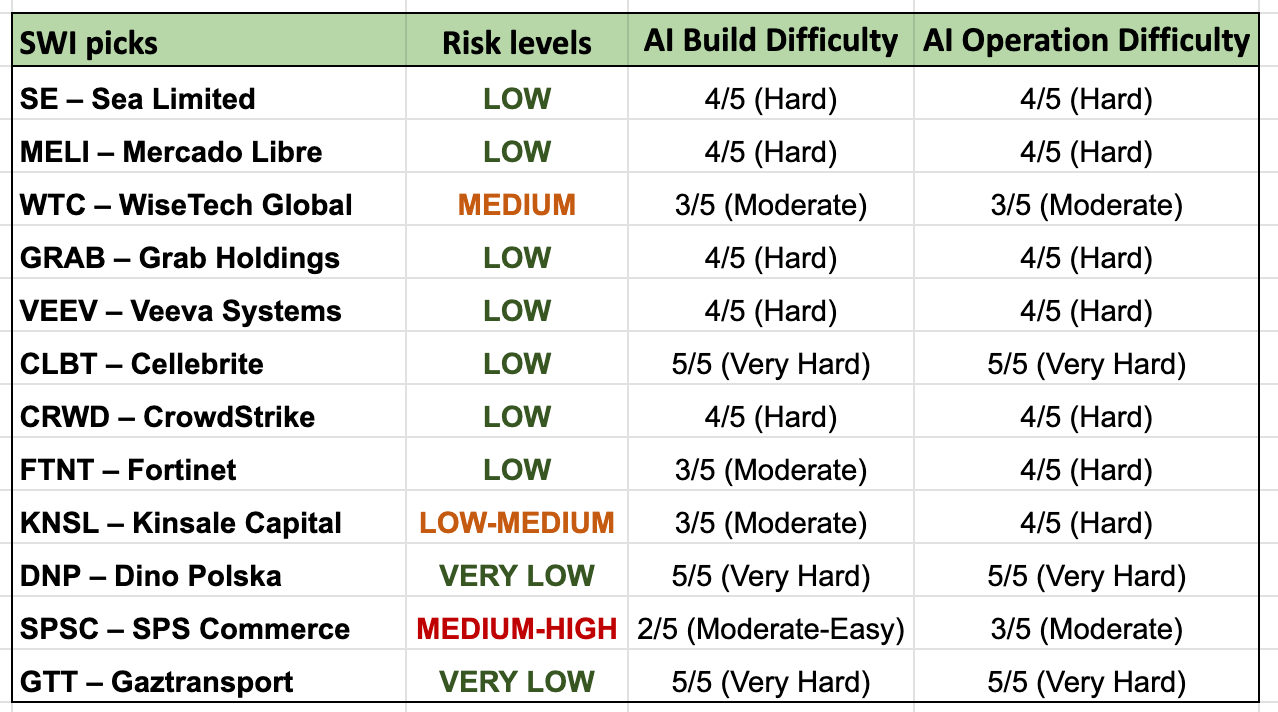

For nine of my twelve positions, AI is actively expanding the value these businesses deliver. CrowdStrike benefits because more AI means larger attack surfaces. Veeva benefits because AI agents operating in biopharma need a validated, compliant data infrastructure. Cellebrite benefits because digital evidence becomes more voluminous and complex. GTT benefits because it is the only viable technology for the LNG infrastructure that powers the AI data center buildout. Dino Polska, Sea Limited, Meli, and Grab operate in physical-world markets where AI is a logistics optimizer, not a competitor. SWI’s AI Risk Assessment

Let’s dive into why I bought more Veeva Systems, and have ordered to buy more Mercado Libre, Cellebrite, and Sea Limited.

This trade alert write-up replaces my monthly Best Buys edition to remove duplications.