SWI Pick #3 - Shimano - Under-appreciated Bike Component Monopoly At An Attractive Price

High quality compounder with 100+ years of history, ~50%+ market share, average ROIC of 22% over 15 years, $3B cash, significant reinvestment opportunity, and trading at a compelling valuation.

Intro to Shimano

Shimano (7309.T, SMNNY) is the world's largest bike component and second-largest fishing tackle manufacturer, with ~50 percent market share for all parts (~70 percent market share in mid-high-end components). It was founded in 1921 by Shozaburo Shimano in Sakai, Osaka. The company's first product was the single freewheel, and through a century of incremental improvements, it has become the foundational mechanic and the most technical component of bikes today. Impressively, it's still run as a family business at ~$5B in sales and ~$15B market cap (~$12B enterprise value). The grandson, Yozo Shimano is the current CEO, Taizo Shimano is the President (the 5th), and two other Shimano family members as executive directors. The company was listed on the Osaka Securities Exchange in 1972 and has returned 10x since 2000.

The investment case in Shimano is two-fold. It is a proven productive and anti-fragile business that will likely endure the test of new competition in the e-bike segment and current macroeconomic turbulence. This is a high-quality business and rarely trades cheaply. However, after falling 40% from its peak in September 2021 to Y21,000/share on the JPX Tokyo Stock Exchange (or ~$16/ADR share in the OTC market, ticker: SMNNY, 10 ADR shares equal one share), I believe the base case valuation at $23/ADR share (7%WACC, or $20/ADR share at 8% WACC) presents an attractive BUY rating with 25% margin of safety. Even in the worst-case scenarios like a decline similar to the 2008 financial crisis, the current valuation provides limited downside.

Shimano scores very high under my sleep well investment checklist, with 14 points out of the possible 20. I am happy to accumulate shares at the current price, targeting a 3% position.

A sleep-well investment

In Shimano, you would own a business that produces the building block of an essential transport mode, bike components (~80% of revenue). You would also invest in an inspiring corporate mission to bring people closer to nature and live happy and healthy life. Shimano has been producing bike components for over a century and fishing tackle for 50 years. It’s hard to imagine these products will disappear anytime soon. People will still want to get from A to B, enjoy life in nature, and, importantly, in an eco-friendly way, which also aligns with the global fight against climate change.

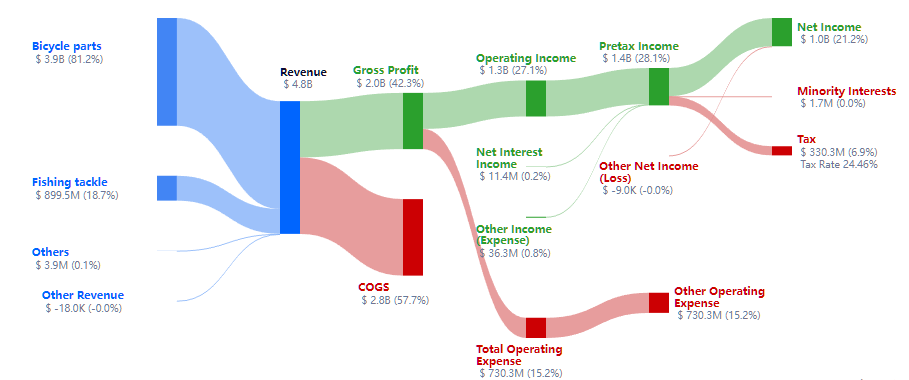

Source: Gurufocus Sankey chart FY2021

Shimano’s business model is also proven and time-tested over many economic crises and industry cycles. One of the underlying reasons is that the bike value chain is very stable and unlikely to be disrupted in the foreseeable future. You have aluminum, plastic, steel, and titanium suppliers at the upstream part of the chain. Then you have the component manufacturers like Shimano, SRAM, Campagnolo, and others. At the end of the value chain, bike brands assemble, sell, and service after the sale. Shimano sits most comfortably as component manufacturing is the least competitive area. The main reason is that the barrier to entry is very high, being the most complex and innovation-intensive part of the value chain; consequently, the high-margin business is well protected. On top of that, Shimano has the most differentiated offerings aiding the longevity of the business model. In detail, Shimano is superior to its peers in four aspects: