Business Update - Mercado Libre (MELI) Q3'24 - Double Down on Fintech and Logistics

Great results: Investments in logistics and credit portfolio favoured over short-term profitability. Shares -16%, I added shares to my PA.

Hi, sleep well investors,

Mercado Libre (MELI), the 16th sleep-well pick, reported business-as-usual Q3’24 earnings yesterday. The company is thinking long-term, reinvesting in logistics and Mercardo Pago to further improve customer value prop, fortify the ecosystem, deter competition, and put the best foot forward to capture the enormous opportunity ahead in Latin America.

As a reminder, only 15% of commerce in the region is done online. In fintech, Meli has an opportunity to capture 125 million unbanked people, half of whom are in Mexico. Thirdly, the enormous advertising opportunity that will keep growing as the ecosystem develops, already at a $1B run-rate, growing at over 50% for the last eight quarters (37% in Q3’24). It won’t be linear, but Amazon has achieved a 40% CAGR since reaching the $1B mark in 2014 to reach $51B annually today.

As a long-term owner, I am delighted with the results. Nothing broken. With shares down 16% post-earnings, I have added shares to my personal account (PA). Do you think I missed something glaring? Tell me in the comment section.

Loyal readers know I don’t play the Wall Street ‘beats and misses’ game, so let’s review Meli through the lens of an owner.

To understand Meli, the risks of Amazon and local players, and the dynamic region - read my deep dive here.

Premium members have benefited from my high-quality research and disciplined portfolio execution. Since going paid last summer,

17 picks have had an average return of 29%. There is only one loser in the portfolio.

Quality > Quantity.

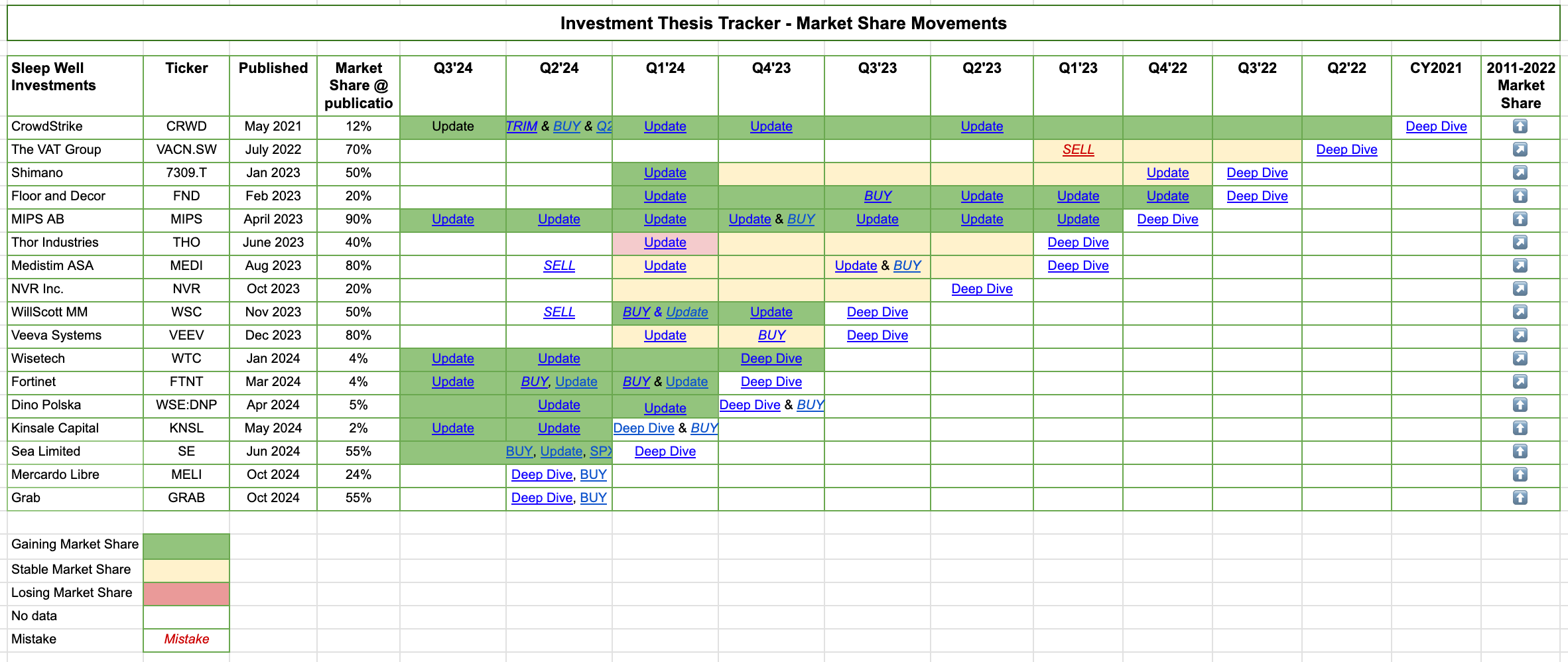

You can track the deep dive performance below. The portfolio update for October is here.

I compile all thesis tracking here and link it in the Sleep Well Portfolio spreadsheet (annual sub only). You can also access all buy-and-sell, and deep dives.

For all sleep-well writeups, please click this link.

Meli Q3’24 results

All investments depend on your story about the business and its environment. I see in Meli an engine of commerce of LATAM running full steam. The engine is made up of frictionless commerce experience, accessible consumer and merchant credits, comprehensive tools for brands, and the most reliable logistic networks. The fuel is the 650M million people in Latin America, of which only 15% of total commerce spending is online, and 125 million still do not have access to essential banking services. Thus, what I want to see every quarter is for Mercardo Libre to remain focused on helping customers get the best out of Meli’s platforms and reinvest just like Amazon in the US and Europe so more people plan their lives on it (spend, do commerce, save, invest, insure).

And what did Meli do in Q3’24?

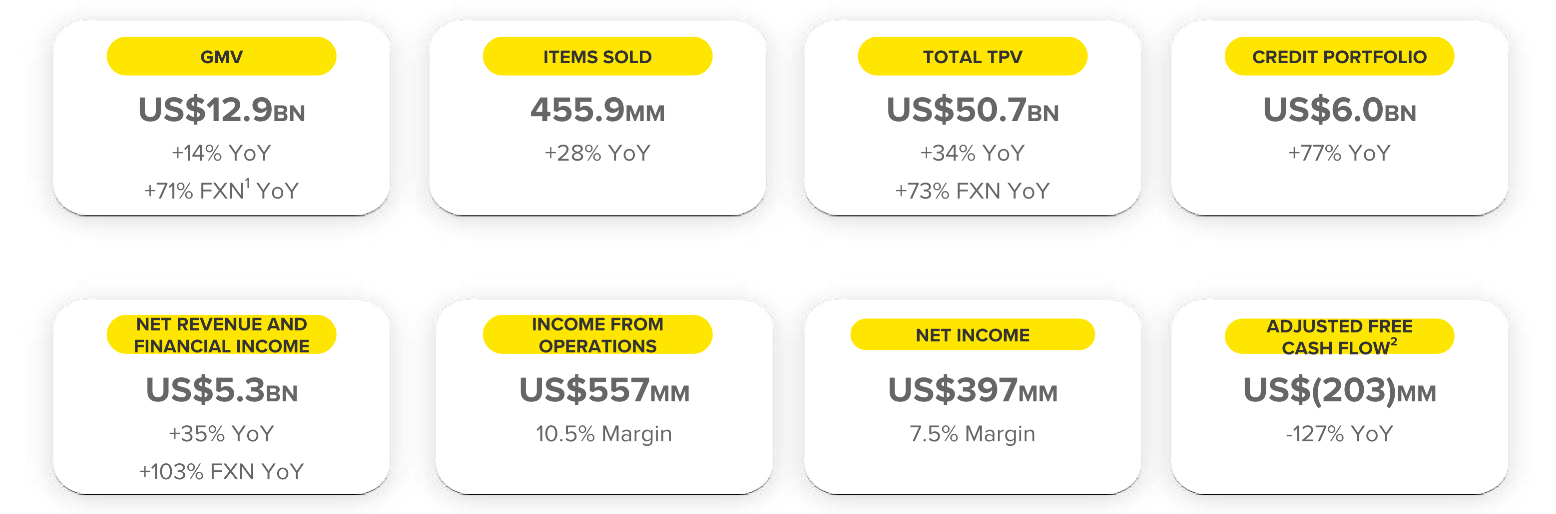

It built out more tools, added a cheaper tier for Meli+ (Amazon Prime equivalent), and added 7 million buyers, reaching 61M, more than the peak of the Covid period.

Invested heavily in logistics; opened six new fulfillment centers, 5 in Brazil and 1 in Mexico, to reach 26 in the region and 16 in Brazil.

Invested in fintech (Pago); issued 1.5 million new credit cards, boosted transaction payment value by 166% YoY, and underwrote more consumer and merchant credits, grew credit portfolio by 77% YoY to $6B. Fintech monthly active users grew 35% YoY to 56M.

GMV grew +14%: Revenue rose +35% (commerce +48% and fintech +21%), Items sold rose 28%, Unique active buyers reached 61M.

As a result of the investments, profitability and cash flow dropped. The operating margin was 10.5% vs. 18% in Q3 ’23 while adj. free cash flow was negative (-$203M, but trailing 12mon is still at a massive $4.5B).

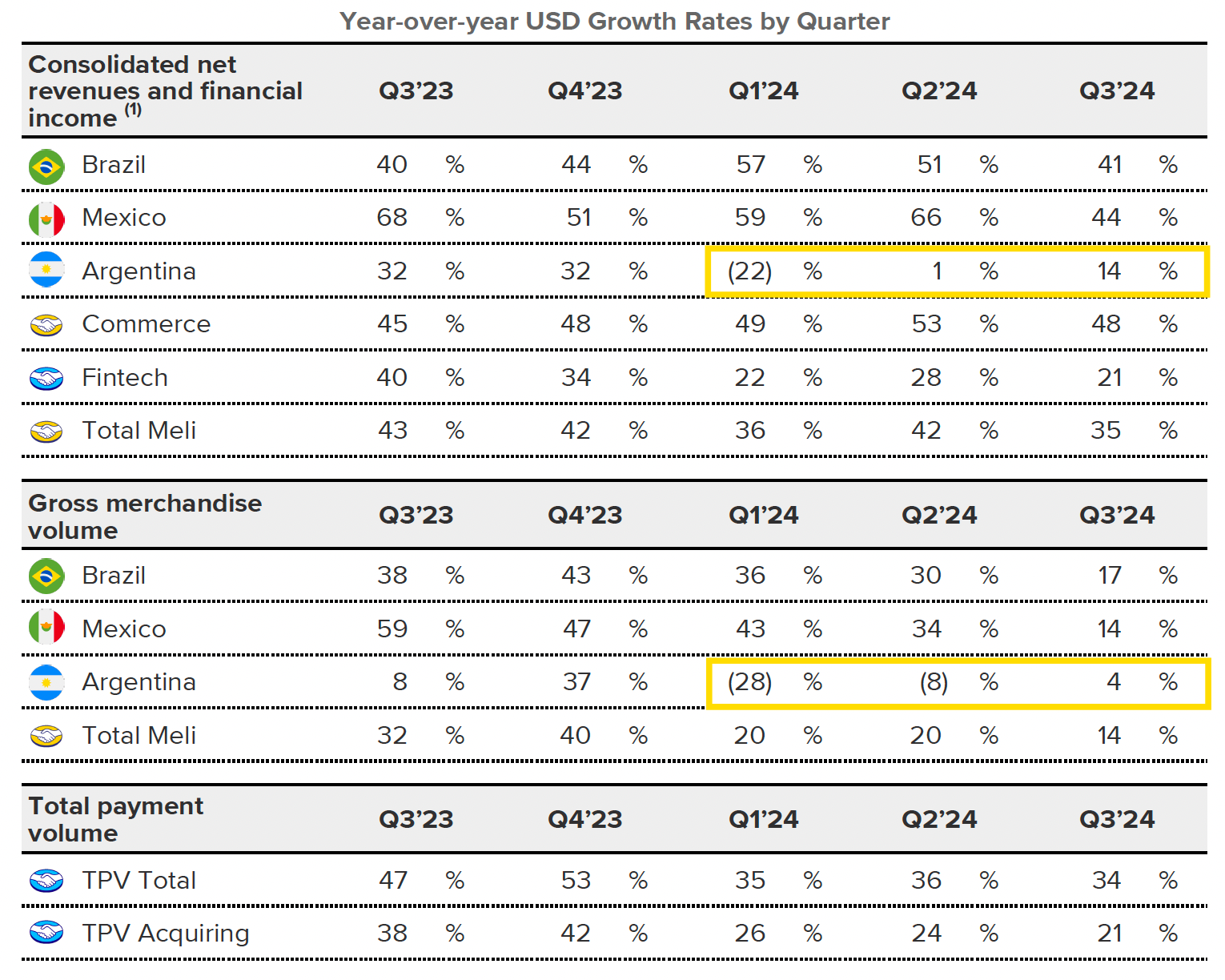

All countries grew, with Argentina returning to growth at 13.5%.

Brazil and Mexico, the two largest markets, grew at 41% and 44%, respectively.

I leave these two tables below for your reference on how each segment performed in different countries.

Let’s discuss why Meli has a firm conviction in logistics, fintech, and advertising.

Logistics - the backbone

Logistics is the backbone of Meli’s commerce. Better logistics equals a better transaction experience, which leads to higher transaction frequency and dilution of last-mile delivery costs.

Higher frequency drives engagement, trust, or ‘addiction’, resulting in better retention and conversion for cross-selling of other products within Meli’s ecosystem. Over the last 10 years of using Amazon, my whole family has gone from just buying odd items to now everyday needs, to work related like laptops, then watching shows on Prime, if it has a digital bank we probably will use Amazon’s as well.

Above is what Meli is building, and it already has the most extensive consumer base and platform for merchants to do business in LATAM. Now, the expanding reliable logistic network will kick up the addiction, driving higher conversion and stronger buyer and seller satisfaction (measured by NPS - net promoter score).

In Q3’24, fulfillment penetration rose by 4.5 percentage points compared to a year ago, and same-and-next-day shipments grew 16% YoY, setting a record with growth accelerating since Q2. The percentage of these fast deliveries slightly declined as more users chose Meli Delivery Day, a slower, cost-effective option — no problem here.

By FY2025, Meli aims to double Brazil's fulfillment capacity to over 20 (11 as of Q2’24 and 16 Q3’24). This shows the huge market opportunity in Brazil alone (good for Sea Limited—Shopee—our other sleep well pick).

Fintech - Mercado Pago

Engagement rose, with "power users" (those transacting in nine out of the last twelve weeks) growing at a much faster rate, and transactions and products per MAU also rising. Fintech MAU reached 56.2M, assets under management (AUM) reached $8B and credit portfolio nearly doubled to $6B.

The credit card business is now 39% of the portfolio, up from 25% last year, driven by the expansion to lower-spread products, the effect of the ecosystem driving faster penetration. This is the core reason why we saw a drop in operating margin: The additional credit card business immediately requires a larger provision of bad debts, which doesn’t reflect the credit portfolio performance.

The core thing to understand is that credits in the past have had stable loss ratios and well-covered provisions, so if these new credits (with lower spread and perceived higher quality) maintain the current loss ratio, profitability from this cohort will look great in a few quarters!

We know that the faster growth of our credit portfolio, combined with the shift towards more credit card as a percentage of total portfolio puts some short-term pressure on NIMAL spreads. Rather stable NPLs that we have seen and the fact that the earlier cohorts of credit cards are already becoming profitable gives us confidence in our investments. - Marcos Galperin Q3’24

Notably, the credit card business drives engagement in other parts of Meli's platform.

So the fact that we are growing so fast and that the recent cohorts represent a significant part of our total portfolio makes -- have a -- has an impact in our returns or in our P&L in the current quarter, and we are very excited with how the product is evolving, not only because all the cohorts are already profitable, but also because we see all of the drivers that the increased penetration of credit cards bring us from higher Net Promoter Scores, higher transactions in users who have credit cards, both in the marketplace, but also off the marketplace, increased use of other Mercado Pago products and in general, an increase in principality.

Advertising

In my deep dive, Advertising is projected to be a $6B opportunity that would add $90B to the current market cap, doubling the company's value.

If Meli can grow its ads business at a 20% rate for the next ten years, that would generate $6B in revenue and $3B+ free cash flow.

At a 30x FCF multiple, the ads segment would be valued at $90B.

Alternatively, if we use the 5% GMV Amazon’s ad take-rate as a proxy for calculating Meli’s ad business, then it would be able to generate $6B of revenue by 2034, assuming a $114B GMV in 2034 growth rate of 10% CAGR.

Q3’24, Meli’s Ads grew 37% YoY and accounted for 2% of GMV. There is lots of room to grow. There are strong reasons to believe it can emulate Amazon’s Ads (and reach 5% of GMV). It could be even better because:

Meli has Mercado Pago, in addition to the marketplace that produces richer relevant first-party data with purchase attributes and big brand data coupled with the most extensive distribution of ads to consumers of many segments and interests (Products: commerce, digital, offline commerce; Channels: displays, media).

Meli has the right testing environment for building an excellent ad business like Amazon in LATAM. Meli’s ad business is built upon the 220M active users and 100M unique buyer behaviors.

The retail Media Ad market in LATAM is far from developed, which is estimated to grow at 12% over the next 5-10 years. Meli is well-positioned to deliver above-market growth as the go-to retail ad inventory marketplace with a 56% market share.

Conclusion

Q3’24 was a business-as-usual quarter. Management invests in the long term and doesn’t worry about what Wall Street wants quarter by quarter. They also don’t give guidance!

As the stock dropped unreasonably, I grabbed some shares for my PA (no change for Sleep Well Portfolio as I don’t have more cash there).

“Every time we have invested in enhancing our customer experience, in the past, we have been rewarded with strong growth and improvements in our market position.”

Marcos Galperín, CEO

Finchat.io, my personal Bloomberg terminal, sponsors this post; join Finchart.io using this link to get 20% off and support sleep-well investments.

In case you missed it, I shared recently:

Thank you for reading. If you have found my content value-added, subscribe and spread the word so more long-term investors can sleep well.

Reminder: How can Sleep Well Investments help?

High success rate stock picks—33% money-weighted gain per pick since Oct 2023 (61% time-weighted).

Deep research of high-quality businesses and regular tracking. Buy and verify.

Free samples of deep dives, tracking updates, and buy alerts.

Free articles on investment framework to help find quality companies and execute with discipline.

Promote yourself to 6000+ stock market investors (47% open rate) — Contact me: trung.nguyen@sleepwellinvestments.com

Great piece — and the thesis has aged well. You bought a 16% selloff in Q3 2024. Q1 2026 gave a 40% drawdown from highs on a 49% revenue quarter, so I did the same.

The numbers since you wrote this: credit book $6B → $14.6B (+87% YoY), fintech MAUs 56M → 82.9M, Brazil items sold +28% → +56%, AUM $8B → $19.9B. Everything you were tracking has compounded. The advertising thesis you laid out — $6B opportunity, 2% of GMV today — is tracking well with ads now growing 73% YoY.

Your point on provisions being accounting mechanics not deterioration has become the central debate. Q1 2026 had 3.9% of margin compression from provisions alone — same dynamic, bigger scale. The book is over-reserved at 103% of >15-day past-due. The cohort seasoning logic you described in Q3'24 is now playing out in Brazil where older cohorts are offsetting new cohort dilution.

Published a full IC on the current setup if useful — same long-term conviction, tighter on the credit watch metrics.

https://substack.com/@wallmanresearch/note/p-199050829