Business Update - MIPS AB: Q3-23 Thesis Tracking, Higher Chance of Recovery In Q4

MIPS fell 10% to SEK 250/share after an expected soft Q3 results - I see slower sales decline and stabilising margin. Long-term thesis intact and share price is attractive today.

I am Trung. I write 10+K words deep-dives on market leaders. I also write Thesis Trackers updates to follow up on their performance. When the right price comes, I buy them for the Sleep Well Portfolio, which I am building for my 4-year-old daughter to redeem in 2037. I disclose the reasoning of all BUY and SELL (ideally never) transactions (1st, 2nd, and 3rd). Join me in building generational wealth.

Hi SWIs,

Welcome to the 300 new subscribers in the last 30 days. Your support allows me to dive deep into niche market leaders and track their performance to take the weight off your investing process. 🙏🙏

This post reviews MIPS AB Q3’23 results.

The next post will be my 9th Sleep Well Investments (next week). It fits my Sleep Well Investments mold because it’s a

Niche industrial market leader with a 50%+ market share and providing solutions for over seven decades.

This business is a circular economy investment whereby materials can be refurbished and reused to prolong their useful life, reducing waste.

There is little industry disruption risk, and alternatives are time and cost-consuming.

The product demand/relevance also benefits from the US restoring manufacturing.

Importantly, the business's intrinsic value is undervalued and deserves a starter position at the current range.

Let’s review MIPS AB Q2’23 results.

MIPS AB is a monopoly in bike helmet safety systems, a compounder in the making.

I am bullish on the business long-term as MIPS has multiple enduring competitive advantages that are hard to replicate. It has compounded revenue by 49% CAGR, earnings by 62% CAGR, and free cash flow per share by 39% CAGR since 2014.

The stock appears expensive on an absolute level and has suffered from the post-COVID pullbacks in demand and slow inventory digestion. But I believe it’s reasonable relative to historical levels and in normal times (if we return to that). I highly regard the business's agnostic technology and distribution strategy, the trajectory of its market share (leading brand for Tour de France teams) relative to peers, and its growth potential (in the Safety market).

On 26 Oct, It reported expected soft Q3’23 results after challenging Q2’23 and Q1’23 results. This quarter, I see a slowing decline in sales and a stabilizing EBIT margin. The management guided a recovery in H2 in previous quarters, and the number suggests they might be right or nearly there.

In Q2’23, the CEO, Max Strandwitz, commented:

[…] Bike retailers in the key US and European markets continued to reduce their inventory levels during the period, as expected.

[…] We assess that the third quarter will continue to be challenging but expect to see a stronger fourth quarter and therefore show growth for second half of the year

In Q3’23, he acknowledged the error in the past prediction, and the message is less concerning.

Inventory normalisation in the bike sub-category has taken longer than what the sector and we ourselves predicted.

Our customers communicate that they see a recovery ahead for 2024. Even if demand from end customers has been lower than during the pandemic-boosted years, sales of bike helmets to consumers are still higher than before the pandemic in most of the major markets

And this is the most important message to long-term investors.

When we analyse data from our major bike channels, we see that despite the impact of inventory corrections, we successfully continued to take market share and increase market penetration of helmet models with Mips’ safety system. We therefore remain confident about our long-term growth opportunities in the bike sub-category once the market starts to normalise.

There is no alternative data point to verify MIPS market share gains this quarter (check Q2’23 review), but the long-term thesis doesn’t change for me.

People will continue to cycle to get from A to B, to exercise, and to be closer to nature, at the same time they want to be safe. Thus, consumers will continue to seek the best bicycle helmets.

As a result, I have no problem waiting for another quarter for the bike market to recover as the business expands to more brands and other greenfield opportunities (the Safety segment).

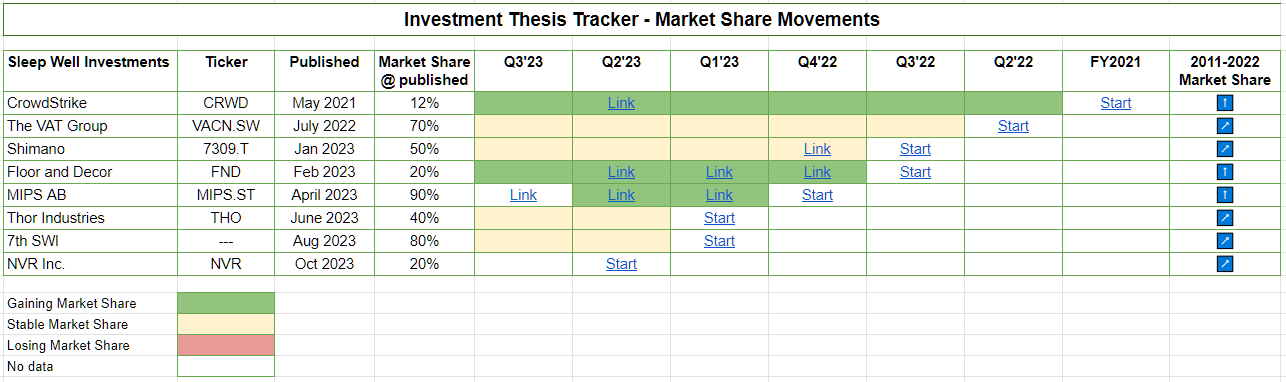

The table above tracks my pick’s thesis and market share each quarter (where data is available), and MIPS’s position remains strong (you will see why at the end of this review).

Another business that will benefit from this secular trend is the industry bellwether, Shimano, a sleep-well business I deep-dived into and own.

Negatives

As I review the headlines, MIPS’s Q3’23 results appear negative but less so than Q2 and Q1.

(-) Revenue continued falling rapidly by 32% YoY to SEK 77M but decelerated from 51% YoY in Q2 and 35% in Q1. Mips customers see recovery in 2024, so we are nearly there (?)

(-) Operating profit margin (EBIT margin) was 19.5%, which seems to stabilize from 23% in Q2 and 17.5% in Q1. This level is far below the 2027 target of 50%, but operating leverage works both ways. As sales recover, EBIT margin should recover very quickly.

The decline in revenue and operating profit was driven by

lower sales in the bike segment (-29% organic sales, decelerating from -52%); but Q3 saw continued digestion of old season models, and MIPS is receiving orders for new ones in Q4.

continued high investments in research and development and marketing (SEK 8M), which was higher than Q3’22 (SEK 6M) despite lower sales.

The market was disappointed, which explains the -10% drop in the stock.

However, in my tweets right after the results announcement and conference call, I don’t see any significant issue.

However, in Q2, the CEO, Max Strandwitz, expected MIPS to return to growth in the second half of the year, with EBIT margin ending around 40%. But both didn’t happen yet. Maybe in Q4, we will see this?

Nevertheless, it’s encouraging to see a stabilizing margin and a slower decline in sales, particularly when Q3 and Q4 are seasonally stronger than Q1 and Q2.

Positives

+ Operating cash flow was SEK 12M, recovering from SEK 9 in Q2 and a negative SEK -42M in Q1’23.

+ Recovery is near. Bike demand is likely recovering in Q4 (management said Q3 at Q1’23 results day and pushed to Q4 in Q2 results), as they see customers return to order new models for the 2024 season despite the grim macro environment.

MIPS helmet sales are split into 50% low range and 30%/20% into mid and high range, respectively. The low range has been the worst-performing segment. As a result, Q1 and Q2 haven’t done well, but management indicates that orders are coming in for the low range (which haven’t been for the last 6-12 months). They see improvements in the second half of the year.

Our customers communicate that they see a recovery ahead for 2024. Even if demand from end customers has been lower than during the pandemic-boosted years, sales of bike helmets to consumers are still higher than before the pandemic in most of the major markets. At Mips we have also substantially increased our customer penetration in recent years with more helmet models equipped with Mips solutions, and we have won new customers.

+ Inventory levels have returned to historic levels.

After a slow start, sales gradually improved during the quarter. Bike retailers in the key US and European markets continued to reduce their inventory during the end of the summer and inventory of bike helmets have now returned to normal levels in the majority of bike stores. Inventory levels at some of our customers in the bike sub-category, the helmet brands, are still higher than normal, but improved during the quarter.

As MIPS is a manufacturing company, most of the sales in FY2023 will come from new helmets for the next season, which will be manufactured in Q4. Thus, the recovery is weighted towards the back end of the year.

The other bright spots are:

+Safety - is showing potential. Revenue grew 482% YoY to SEK 3M (0), accelerating from 439% YoY in Q2 and 300% YoY in Q1’23. MIPS announced two new global brands - MSA and LIFT Safety, which have a strong position in the US safety market in the premium segment. MIPS didn’t report the number of brand partnership changes, but with the two new collaborations, it’s likely 14 (12 from last quarter) if they didn’t lose any.

As the largest total addressable market of 110M helmets annually, MIPS’s future value will depend on how it captures market share in Safety. I’ll be sure to monitor the progress closely. Max Strandwitz expects Safety to contribute SEK 9M by the end of the year vs. 2M for FY2022, a 4.5x growth.

+Investment in Quin - A first strategic investment (25% ownership for SEK 80M) towards exploring the opportunities of sensor technology. The technology will enable MIPS to gather additional data regarding incidents and consumer behavior. I like companies that can grow inorganically, and Quin looks like one.

Capital allocation and cash position

MIPS's only major capital spending was the acquisition of Quin for SEK80M in Q3. Cash and equivalents remain healthy, SEK 371M (498M).

Moats movement

The main reason for tracking quarterly results is to gauge the movement of the business’s competitive advantage and the change in market share. MIPS mentioned winning customers and market share, but I don’t have any available data this quarter to verify, so I leave a ‘no data’ in the thesis tracking table below.

I also see no notable change in the business, so I keep my Sleep Well Investment score for MIPS at 13/20. Perhaps adding an extra point for a more attractive valuation, but I’ll leave it for another quarter to see how the inventory recovery progresses. You can check out my framework for evaluating each business here.

Long-term target and thesis on track

As a reminder, with large untapped markets, MIPS aims:

To triple its annual revenue to SEK 2B and expand its EBIT margin to over 50% by 2027, an upgrade from SEK 1B and a 45% EBIT target by 2025 set in 2021. It will require MIPS to grow at a 40% CAGR in the next five years, achievable compared to the 50% CAGR it has done in the past decade.

The management remains confident in achieving the long-term target. And I am now less convinced they will make it as the year's slow start is due to demand (grim macro) and Covid-unwinding.

I see a company still winning brands, gaining market share, and committed to reinvesting for the future. The Tour de France stats were encouraging and showcased MIPS's brand power.

Over 70% of male competitors’ helmets and 87% of female competitors were equipped with MIPS safety components. Q2’23 commentary

My channel check in Q2’23 confirms that MIPS remains the dominant helmet brand for the 2023 Tour de France.

Valuation

This quarter, the valuation is looking more reasonable as the stock drops.

The initial market reaction lowered the share price to SEK 250/share.

My original buy price was SEK 430/share (read my deep dive here for full valuation workings and assumptions).

Today's share price provides a sufficient margin of safety, so I am happy to buy some and will update the transaction in the Sleep Well Portfolio.

Stay tuned for my future updates on MIPS and my additions.

My next pick will be a small-cap market leader in a niche industrial segment with over 50% market share, recurring revenue, and opportunities to reinvest organically and inorganically.

The best of Sleep Well Investments

I cover a range of sectors that are least likely to lose relevance, including semiconductors, bike and helmet components, RVs, surgical equipment, cybersecurity software platforms, home building materials, and more. You can find all the topics that we cover here.

CrowdStrike - Cloud security leader +27% CAGR since IPO

The VAT Group - Vacuum valve leader +32% CAGR

Shimano - Bike component leader +12% CAGR

Floor and Decor - Future leader in hard-surface flooring +30% CAGR

MIPS - Helmet safety leader +45% CAGR

Thor Industries - RV leader +14% CAGR

Medical device leader +17% CAGR

NVR - Top US East Coast Hombuilder +30% CAGR

My investment philosophy

Being optimistic and patient are superpowers.

I’m a business-focused investor with a long time horizon.

I invest in a business to own it. I rarely ever sell. Instead, I stop adding to positions that turn against me.

I hold about 20 stocks at a time. I start with small positions and let the portfolio concentrate over time without rebalancing. I invest when the price is right and add fresh savings to the stock market across large caps and individual stocks.

My investment moto is:

Study market leaders.

Track them thoroughly.

Own them for decades.

What makes a business leader in their market?

I hope we can figure it out as we break down their business and track their performance together!

Sponsorships

Interested in collaborating? Sleep Well Investments is read by decision-makers across finance, tech, and business. That includes the C-Suite of public and private companies, funds, family offices, and CIOs worldwide.

We'd love to hear from you if you want to learn more. Send us a note at trung.nguyen@sleepwellinvestments.com, and we’ll respond!

Affiliate partnership

Use ‘SWI20’ code at checkout for discounts - Quartr is a searchable database of slides, interviews, and earnings calls. It helps me to gather relevant and valuable insights efficiently.