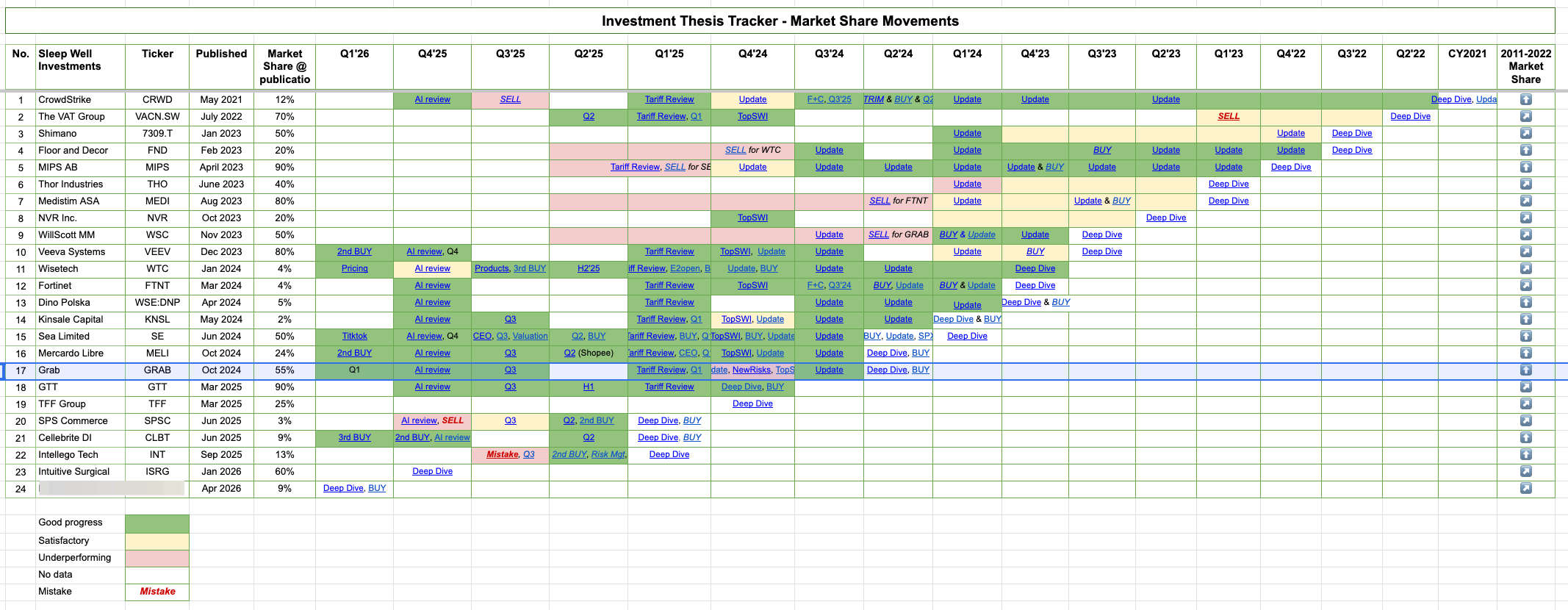

Grab Q1'26: Profitable Growth, Reasonable Valuation

Despite the fuel crisis, commission cap, business did well across the board.

GRAB, a position acquired in October 2024, reported very good Q1’26. We see a clear sign of operating leverage as the ‘land and expand’ strategy continues.

In this report, I dive straight into four underlying growth drivers that require owners’ attention.

Before you start, you can skim through the Q1’26 results here — I won’t discuss the obvious. We will focus on:

Drivers and customers’ incentives, fuel prices, and commission decree.

Financial services reinterates breakeven by H2’26 - showing risk control

Advertising monetization - active advertiser growth slowing, durable average spend growth

Capital allocation showing positive direction - $5B cash position.

Positioning to future-proof from AI and AV.

Then we’ll revisit why Sleep Well owns Grab and whether a ~20x free cash flow valuation (~10B EV) is attractive/unattractive for the Sleep Well Portfolio.

Read our previous write-up on Grab for more context.

Q3’25 - Earning update

Q1’25 - Tariff Review, Q1 Update

Q3’24 - Update

Disclaimer

As a reader of Sleep Well Investments, you agree to our disclaimer. Full details here.

If you are new to SWI, check out our FAQ and Owner Manual.