Business Update - Grab Q3'24: Super App Growing Sustainably

Grab reached 42M users, profitable for two consecutive quarters, $500M forward FCF makes this business 25x EV, reasonable for the 15%+ 10 yr CAGR.

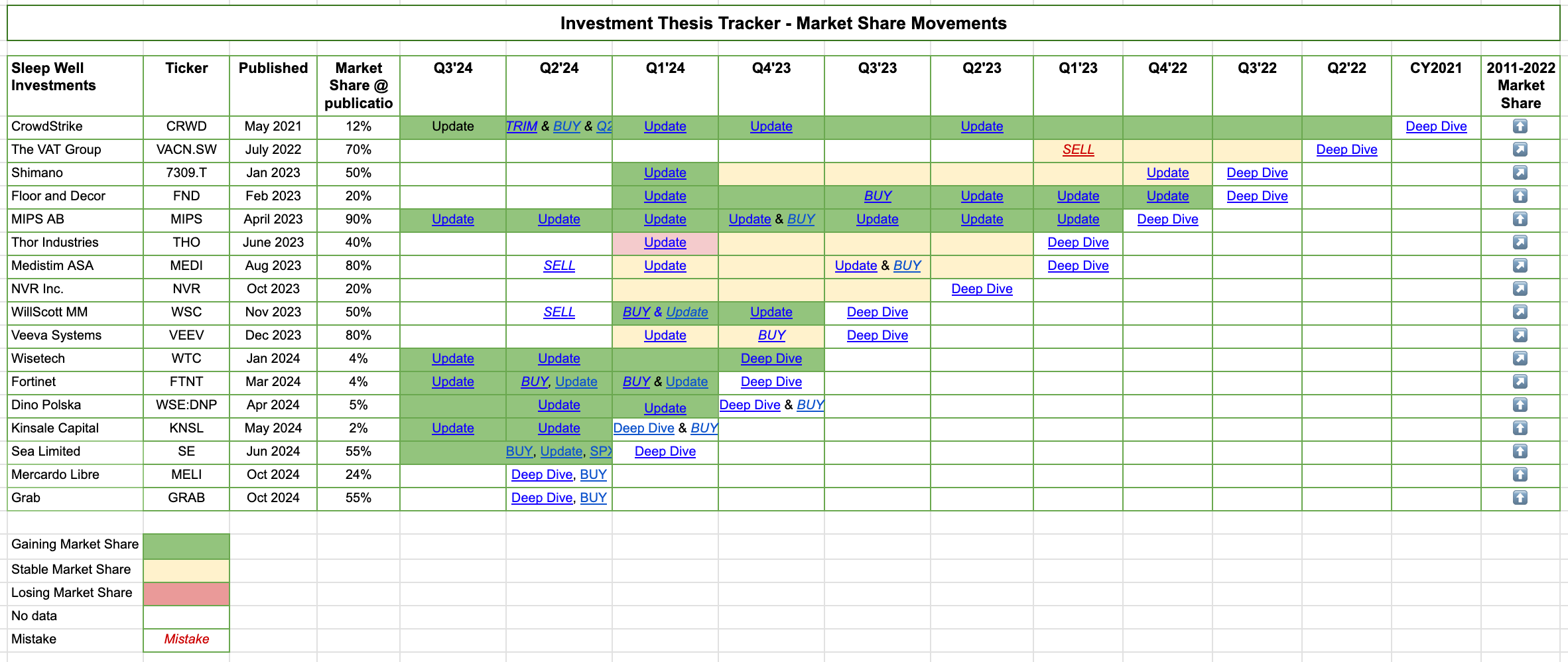

Hi, I am Trung. I deep-dive into market leaders that passed my sleep-well checklist. I follow up on their performance with my Thesis Tracker updates, and when the right price comes, I buy them for the Sleep Well Portfolio, which I am building for my daughters to redeem in 2037. I disclose my reasoning for all BUY and SELL (ideally never). Access all content here.

Hi, sleep well friends,

This post updates Grab’s Q3-24 thesis (and reviews its direct peer - GOTO). Read my deep dive last month to learn about the business and why I bought it for the Sleep Well Portfolio. I recommend reading Sea Limited and Mercado Libre to appreciate the strength of the marketplace model in different regions.

Q3’24 results are going full steam; all positive so far. I have reviewed

MELI Q3’24 [FREE],

MIPS, KNSL Q3’24, WTC’s CEO reshuffle, and the FTNT + CRWD partnership.

Dino, FTNT reported and will be looked at.

The Sleep Well Portfolio looks strong, up 34% per pick on average.

All other thesis tracking can be found here and linked in the Sleep Well Portfolio spreadsheet (annual sub only). You can also access all buy-and-sell, and deep dives.

As a reminder, I focus on the long-term story/execution of the business, not the quarterly Wall Street beat/miss quarterly records. So, my thesis tracker primarily checks how my picks build their value propositions, cope with adversity, and maintain/grow moats and market share.

For all sleep-well writeups, please visit this link.

Grab Q3’24 - November 12th

Briefly, Q3’24 showed strong growth in core segments (deliveries and mobility) driven by increased frequency and higher value transactions; fintech continued rapid adoptions, resulting in solid Adj. EBITDA guidance for FY2024. Valuation remains cheap with 25x EV/Forward FCF ($500M free cash flow run rate) despite shares likely hitting $5 or $18B market cap and $13B enterprise value (EV).

If you are new, Grab is a Southeast Asian (‘SEA’) super-app with a 55%+ market position in deliveries (foods, groceries, beauty, etc) and 50%+ in mobility (taxis). The company has been operating unchallenged across SEA after beating Uber in 2018 (6 years after its founding), except for Indonesia, where Gojek (GOTO) is neck and neck. Covid disrupted Grab’s growth with prolonged lockdowns. Still, since reopening, Grab has been capturing market shares, reaching profitability, and leveraging its scale to expand successfully to Fintech products (digital bank accounts, loans, investment, BNPL, insurance). Financially, it is poised to post the first year of free cash flow at a $500M free cash flow run rate - after burning nearly $5B five years prior. The company has a long way to go to grow profitably, with 2/3 of SEA still underbanked.

Q3’24 was another step in the right direction - showing growing demand and increased stickiness of the super app.

Let’s go over the key metrics:

Core growth

GMV (deliveries + mobility) +15% to $4.6B above the 10%+ industry rate

Monthly Transacting Users + 16% to 42M

Partner and customer incentives of % of revenue +14% and +27% are high but should decrease as habits crystalize in the next few years, showing margin expansion potential.

Key long-term growth

Fintech - bank deposit +300% to $1B (mainly in Malaysia and Singapore, and loan underwritten +38% to $567M ($2.2B run-rate) with a 2% loss ratio.

Advertising - +78% to $50M at 1.6% of Deliveries GMV from $28M last year at 1.1% of GMV and 1.4% in Q2’24. Best: driven by a self-serve high-margin model (The Trade Deskesque) with little need for an account manager. Uber generates Ads revenue at 1.6% of total GMV, so there is room for Grab to expand.

Profitability and cash flow - a huge inflection

Deliveries Adj.EBITDA as a percentage of GMV was 1.8%, up from 1.3% YoY (long-term target 4% - management)

Mobility Adj. EBITDA as a percentage of GMV was 8.8%, down from 9% YoY (long-term target 8% - my assumption)

Fintech Adj. EBITDA losses narrowed to $26M from $36M

Group Adj. EBITDA up 3x to $90M after corporate costs.

Free cash flow reached $137M, making it the second quarter of FCF positive, with a run rate near $500M.

For context, Grab burned nearly $5B between 2019 and 2023, 2023: -6M, 2022: -$900M, 2021: -$1B, 2020: - $700M, and 2019: - $2B. This is a huge inflection point of free cash flow.

Cash level - $4.5B

The cash war chest is now a third of the market cap. The $6.1B cash liquidity below includes the $1B deposit from the customer but is earning interest income for Grab.

$4.5B is cash deployable for the business. This is high for my liking, but it’s a good problem as Grab still has over $300M (of the $500M authorized) allocated to buy back shares (it bought 189M shares so far at $3.3/share), a buffer for the chance of higher non-performing loans, and firepower to compete and improve the ecosystems. Optically, it also deters entrants.

Segments focused commentary

My thesis on Grab is that with the moats it possesses (see deep dive), over the next 13 years, growth for core platforms should sustain between 5-9%+, further boosted by Fintech +28% and Advertising +32% to possibly 12%+ CAGR as a group. If Grab achieves this level, I believe Grab should be a much bigger company, but if someone puts a gun to my head, a number I have in the deep dive model is approximately $7/share.