Business Update - Sea Limited (SE) - Q2'24 review - Building an Evergreen Franchise

Garena looks more like an enduring cash-cow, Shopee maintains dominance and turning profitable in Q3, SeaMoney is executing prudently. I am still a buyer at 21x FCF and at 52-week high.

Hi, I am Trung. I deep-dive into market leaders with my sleep-well checklist. I follow up on their performance with my Thesis Tracker updates, and when the right price comes, I buy them for the Sleep Well Portfolio, which I am building for my daughters to redeem in 2037. I disclose my reasoning for all BUY and SELL (ideally never). Access all content here.

Hi Sleep Well Investors,

The transformation Sea Limited made post-COVID is showing incredible results (deep dive, buy alert). The three segments are growing at a 20%+ rate with an improving bottom line. Together, they generate roughly $1.9B of free cash flow (Garena: $1.2B, Shopee $0, and SeaMoney $660M) annually, contributing to an already healthy $9B cash balance.

The only pickle in Q2’24 was no mention of the India relaunch (no analyst asked the question!). However, the thesis is still a massive upside in increasing take rate, particularly in the Ads segment, improving moat in logistics, and SeaMoney's durable 20% growth.

Below are the key highlights, followed by deeper commentaries.

Three standout highlights:

Garena is an evergreen enterprise with 100M daily active users (648M monthly active), and Firefire continued to be the most downloaded mobile game globally in Q2. Investment in Garena’s game-creating tools is an excellent step to reduce reliance on Firefire.

E-commerce dominance - take rate increasing, logistics improvements, positive EBITDA from Q3, ads upside, limited competition from TMall and Temu.

SeaMoney saw 40% growth in loans to $3.5B and 58% in customers to 21M while improving the loss ratio.

Before we discuss each segment in detail, I’d like to ask you to spread the word so that more long-term investors like you can benefit from Sleep Well Investments’ high-success-rate research.

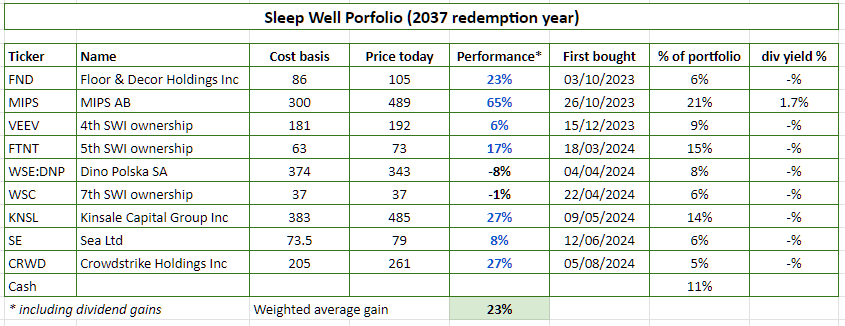

So far, the nine buys have made an average return of 23%—no significant losses.

The biggest win was selling CrowdStrike at $381/share to buy Sea Limited a month ago and then rebuying CrowdStrike at $205/share (pairing with adding to Fortinet as a hedge) after CrowdStrike demonstrated sufficient evidence for me to believe it is owning the mistake and executing steps to change for the better.

Of all the recommendations, even buying without considering valuation or following my buy alerts has had an average return of 20%, with only three notable losses. Again, the result shows that you will likely sleep well here.

Above, you can still achieve good results without investing in the Amazon of the world, where you can get coverage from 100s of analysts anyway. I am all about finding less-covered businesses, observing them patiently, and buying at a reasonable price so you can enjoy an edge before the significant funds. I spend 100% of my time researching sleep-well businesses and executing my buys/sells with discipline.

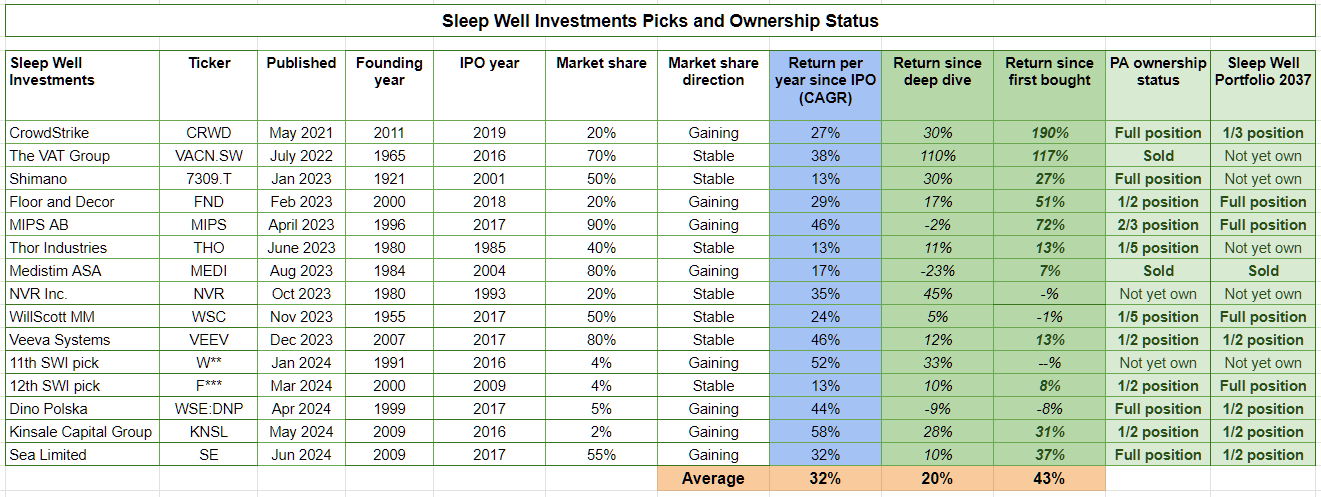

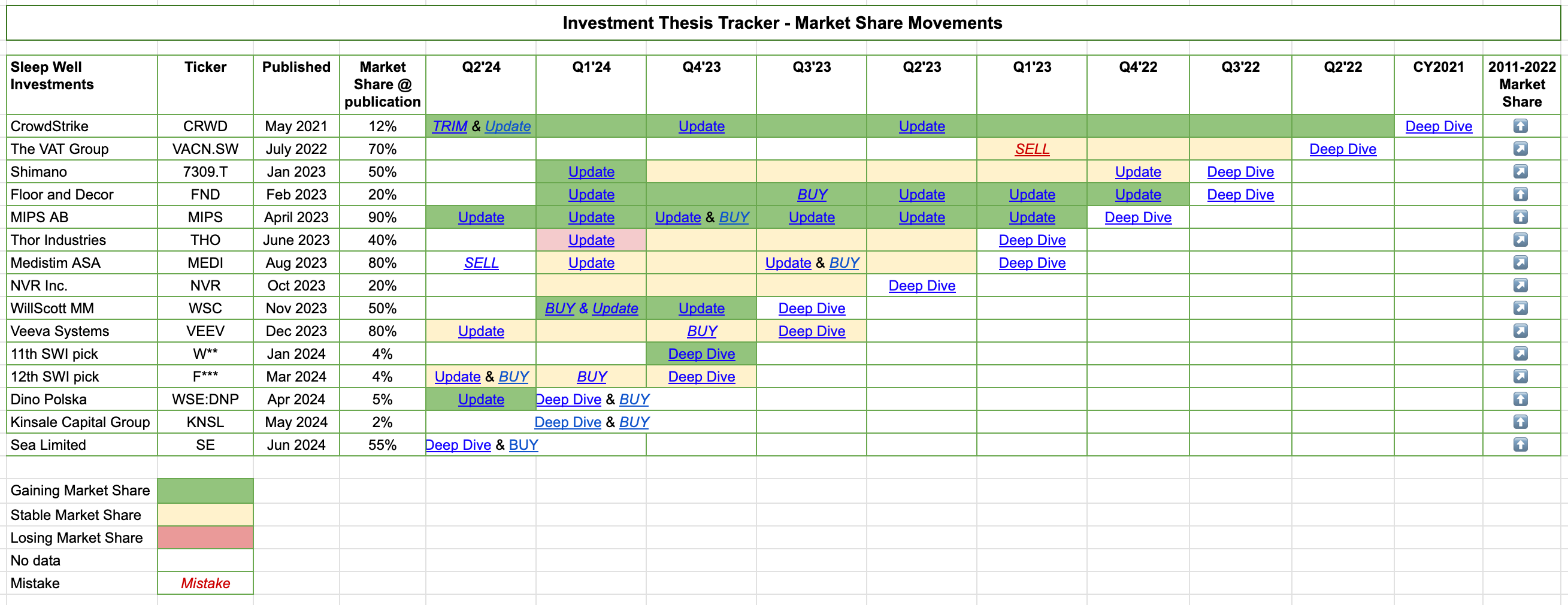

Below is the timeline of my deep dives, tracking, and buys. All-access is in my spreadsheet and is available to annual members.

If you are new, here is

how I select my sleep-well businesses, and

how I construct my Sleep Well Portfolio.

how I track my businesses