Business Update - Thesis Tracking Q3'24: Floor & Decor, WilScott, Dino Polska

FND coping well, WSC McGrath deal not closed yet, DNP.WA opening more stores.

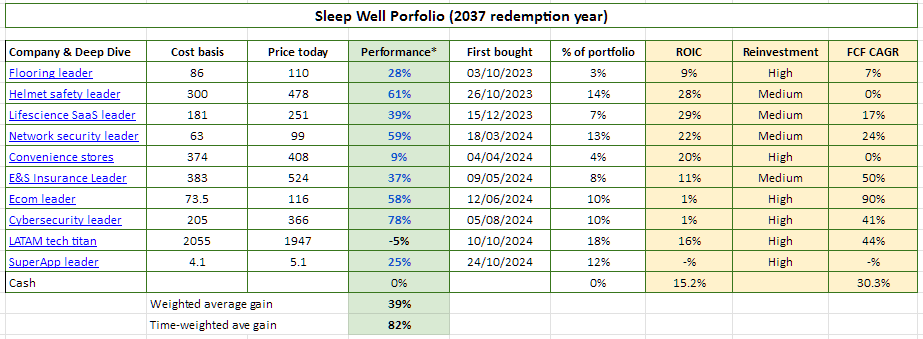

Hi, I am Trung. I deep-dive into market leaders that passed my sleep-well checklist. I follow up on their performance with my Thesis Tracker updates, and when the right price comes, I buy them for the Sleep Well Portfolio, which I am building for my daughters to redeem in 2037. I disclose my reasoning for all BUY and SELL (ideally never). Access all content here.

Hi, sleep well friends,

This post tracks 3 of the 17 sleep-well picks:

Floor & Decor (FND) - Coping well with slow existing housing sales.

WilScott MM (WSC) - Is the McGrath deal closing? Trimmed for Grab.

Dino Polska (DNP.WA) - Reacceleration in store opening

Next, I’ll review

VEEV - life science leader, up 40% since bought (Dec 2023)

FTNT - network security leader, up 60% since bought (Mar 2024)

CRWD - endpoint security leader, up 78% since bought (Aug 2024)

WTC - logistics SaaS leader, up 88% since picked (Jan 2024)

I compiled all thesis tracking here and linked it to the Sleep Well Portfolio spreadsheet (annual sub only). You can also access all buy-and-sell notes, and deep dives.

Previously, you can read Q3’24 reviews of:

SE - SEA e-commerce leader, up 58% since bought (Jun 2024)

MELI - LATAM e-commerce and banking leader, down 5% since bought (Oct 2024)

GRAB - SEA Super App leader, up 25% since bought (Oct 2024)

MIPS - helmet protection leader, up 61% since bought (May 2023)

KNSL - E&S insurance leader, up 15% (May 2024)

WTC - CEO shakes up, logistics SaaS leader, up 88% (Jan 2024)

FTNT + CRWD partnership of endpoint and network security leaders, up 26% and 48% (Mar & Jun 2024)

As a reminder, I focus on the long-term story/execution of the business, not the quarterly Wall Street beat/miss quarterly records. So, my thesis tracker primarily checks how my picks build their value propositions, cope with adversity, and maintain/grow moats and market share.

Current Sleep Well Portfolio holdings:

For all sleep-well writeups, please visit this link.

Finchat.io, my personal Bloomberg terminal, sponsors this post; join Finchart.io using this link to get 20% off and support sleep-well investments.

FND Q3’24: Coping well with macro challenges and slowing store opening, FY24 will end at 251 stores.

Floor & Decor’s primer

Floor & Decor (FND) is a hard-flooring warehouse retailer with a 9% market share, operating 251 stores across the US (FY24 est.). It has the best value proposition for professionals (breadth and depth of in-stock SKUs), scale advantage, and a clear capital allocation plan to widen moats and win market share. At maturity (450 stores in 10 years - my base case), I estimate that FND could command a 25-30% share of the market on the basis that industry leaders Home Depot and Lowe’s fail to keep up with FND’s focus and scale; meanwhile, the demand for hardwood flooring will continue to support long-term industry growth—median US house age is 44 years old. FND has high visibility in expanding revenue by 10%+ CAGR and EBIT by 15%+ CAGR in the next ten years.

Read my deep dive and Q1’24, Q2’23, Q1’23, and Q4’22 reviews for more information.

Keeping things simple, I ask two key questions every quarter:

Can Floor and Decor continue to provide the best value for pro customers and take market share from Home Depot and Lowe’s?

How many stores can it open by 2032 and how will the unit economics unfold?

Everything else is secondary.

Q3’24 results

FND is suffering on first look, with flat revenue growth and a -6.4% same-store sales decline after years of +25%+ and 20%+ organic growth, respectively. It also looks pretty bad lately compared to HD and LOW’s -1.2% and -1.1% decline (with caveats).

Store openings have also been slower than the 20% CAGR guided in 2022. FY24 will likely end with 251 stores, representing just 13% store growth.