Business Update - MIPS Q4'24 - Ambitious Target Pushed to 2029. What Now?

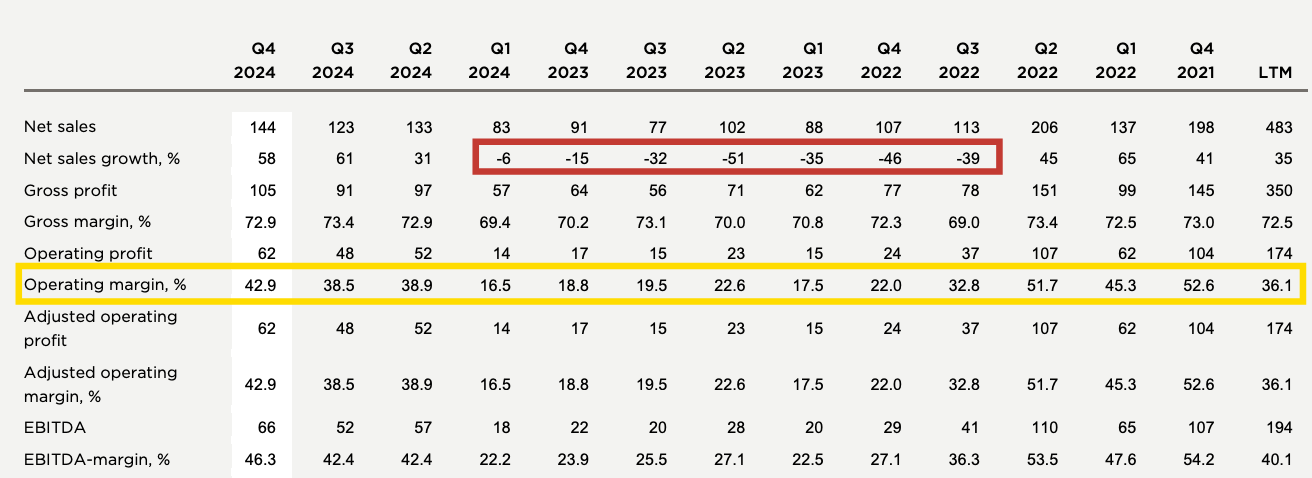

MIPS has truly recovered from the Post-Covid woes, revenue grew 58%, operating margin roared back 43%, but exposed mgt mishaps/shrewdness depending on your side.

Hi, I am Trung. I deep-dive into market leaders that passed my sleep-well checklist. I follow up on their performance with my Thesis Tracker updates, and when the right price comes, I buy them for the Sleep Well Portfolio, which I am building for my daughters to redeem in 2037. I disclose my reasoning for all BUY and SELL (ideally never). Access all content here.

Hi, sleep well friends,

MIPS, a brain-protection component in helmets producer, has been on an incredible roller coaster. It started at SEK 300/share pre-COVID and rocketed to SEK 1200/share at peak COVID in Q4 2021. Then, when inventory was slow to digest in 2023, it crashed to SEK 250/share. It has now rallied back to the SEK 550 region. You could say MIPS is a ‘cyclical’ stock. But I believe MIPS deserves a bit more merit.

Kudos to the company. During the downturn, which lasted seven quarters, not one quarter, MIPS burned cash or suffered a loss—the lowest quarterly operating margin was 16%! That speaks volumes about the company's quality, and I have documented every move during these challenging times.

Read more here: buy alert (at SEK 300), earnings reviews, Q3’24, Q2’24, Q1’24, Q4’23, Q3’23, Q2’23, Q1’23. deep dive.

In 2024, it recorded revenue growth of

-6% revenue decline in Q1,

31% revenue growth in Q2,

61% in Q3 and now

58% in Q4 to end the year with 35% FY2024 growth

Cashflow recovered to pre-COVID levels at ~SEK 87.

Both the top line and bottom line have recovered from the worst. Importantly, it proves that the bloated inventory issue was temporary, albeit for seven quarters.

With better visibility, management has chosen the right time to communicate the lower guidance. It must grow at ~35% annually until 2029 to meet the new target instead of 50% to meet the target in 2027.

Targets in 2029

SEK 2B

EBIT margin >50%

>50% dividend of annual net earnings

The reduced growth rate makes it more possible. For context, MIPS recorded a 50%+ growth CAGR between 2014 and 2022.

With all the trouble over and share recovered. Where do we stand now?

Fairly priced.

At ~SEK 550/share or SEK 14B, MIPS is valued at 7x Sales and 18x earnings if the target is met in 2029. Roughly, if they achieve half of it, then MIPS will be valued at 32x earnings. Depending on how you see the business going forward. It’s either valued reasonably or cheaply. I am less keen to add shares here.

What will make me enthusiastic again?

Safety and Moto need to impress.

Growth in Asia needs to show up.

New channels to leverage MIPS IP.

The bottom line is MIPS is cyclical at the top (revenue) but very stable at the bottom (profitability).

It is still an exceptionally asset-light business with the surprise factor in the upcycle and limited expenses in the downturn. It enjoys multiple enduring competitive advantages that are hard to replicate — agnostic safety technology and a clever distribution strategy that won 90%+ of manufacturers.

At its core, MIPS is the industry standard and only recruits good helmet brands to use its technology. They compete on quality (choosing the right partners), not price or volume. That maintains durable brand equity and relevance.

MIPS already controls most of the market share as viable peers struggle to replace it. MIPS remains the leading brand for 18 Tour de France teams out of 22 and 97/100 top helmets (18 and 91 in 2023).

Summary

MIPS already holds a significant position in the Sleep Well Portfolio, and observing the improvement (and deterioration) of its universal appeal and moats over the last nine quarters has shown me that it still has a chance of being a future compounder.

The long-term thesis remains intact (resilience business, mediocre competition), but I am less interested in adding shares today due to low growth visibility and unattractive valuation.

Current Sleep Well Portfolio:

The Q4 ’24 earnings season has begun. I compile all thesis tracking here and link it to the Sleep Well Portfolio spreadsheet (annual sub only). You can also access all buy-and-sell and deep dives.

As a reminder, I focus on the long-term story/execution of the business, not the quarterly Wall Street beat/miss quarterly records. So, my thesis tracker primarily checks how my picks build their value propositions, cope with adversity, and maintain/grow moats and market share.

For all sleep-well writeups, please visit this link.

Finchat.io, my personal Bloomberg terminal, sponsors this post; join Finchart.io using this link to get 20% off and support sleep-well investments.