5 Timeless Lessons From Terry Smith

Terry Smith's timeless teaching for long-term investors

Hi, I am Trung. I deep-dive into market leaders that passed my sleep-well checklist. I follow up on their performance with my Thesis Tracker updates, and when the right price comes, I buy them for the Sleep Well Portfolio, which I am building for my daughters to redeem in 2037. I disclose my reasoning for all BUY and SELL (ideally never). Access all content here.

Hi, fellow sleep well investors,

I hope you are enjoying Sleep Well’s 33% average return per pick since October 2023.

Sleep Well Investments was initially built on the ideas of three wise investors:

Anti-fragility borrowed from Nassim Taleb,

Irreplaceability from Anthony Deden,

Mundanity from Matthew McLennan.

Over time, I have continued to seek the right investing knowledge from others.

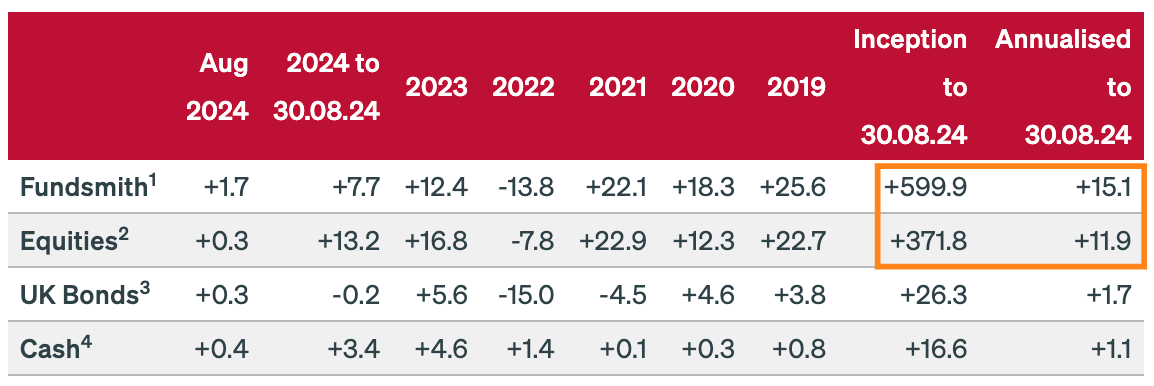

Today, I want to bring your attention to Terry Smith's timeless wisdom. He is the fund manager of Fundsmith, which has compounded 15.1% return vs. 11.9% of the index since 2010.

He is often known as the British Warren Buffett. You can read his famous Owners Manual here and Top 10 Holdings here.

To keep it simple, I have summarised my learning into FIVE points.

Buy great businesses and let them do the compounding.

Choose the quality of the business over the cheapness of stock.

Return on invested capital is a better value creation metric than earning per share.

A high reinvestment rate at a high ROIC is better than buyback and dividends.

Pay up for quality; it’s worth it. (hardest lesson)

1. Buy great businesses and hold on long enough for them to deliver the benefits of their investments.

Great businesses can consistently create value by generating positive returns on invested capital (ROIC) above their cost of capital (WACC). As they can reinvest their excess cash effectively, their ability to earn increases, making them more resilient in economic downcycles. On the contrary, bad companies destroy value because their return on capital is negative, i.e., every dollar they invest loses more money.

‘Buy great business and hold on to them’ —sounds easy, but there are caveats.

Firstly, you must hold them long enough for their investment to bear fruit.

Secondly, a business generating high ROIC quickly attracts competition and invariably finds its ability to earn a high return on investment eroded. Thus, at Sleep Well Investments, we go the extra mile to track and analyze competition and determine if our picks can sustain high earnings long-term.

One of our most recent examples is Sea Limited [deep dive, buy alert, latest update]. Even though it is already the eCommerce leader in Southeast Asia with a 50% market share and the largest online gaming publisher in the region with 650M quarterly active users, Sea Limited is still reinvesting most of its excess cash flow in its fintech division, SeaMoney, and its in-house logistics, SPX, to provide frictionless commerce, superior cost savings, and quality services compared to competitors (old guards: Lazada, Tokopedia, Tiki, and new entrants: Temu, Tiktok).

So far, the investment is working. The fintech arm is already generating $660M of free cash flow, a third of the total amount, and there is roughly 300M unbanked users in the region to capture, what’s better than leveraging its gaming and e-commerce leading market position. Meanwhile, the logistic investments since 2019 have made it the second-largest third-party logistic player behind J&T.

I believe Sea Limited has ample opportunity to reinvest efficiently. Management has proven capability and owns enough shares to lose sleep if they don’t. Still, as Terry Smith noted, the hard part is to keep owning [and verifying] the business until we see SeaMoney and SPX generate free cash flow durably and consolidate as the dominant force in the region.

2. Quality > Value

The next lesson I learned from Terry Smith is to favor the business's quality over the stock's cheapness.

For many years, I did the opposite, buying companies at a cheap valuation and believing that one day, their share price would revert to the means, the business would turn around, or the management would make some miraculous changes. Some did, but in hindsight, perfect timing was required to succeed.

The reality was that these businesses were cheap for a reason, especially when they were cheap over an economic cycle. They have no moats over competitors (scale, network effects, switching cost, brand), operate in industries that consumers can defer buying during downturns (like leather jackets), or have a business model that offers little control over pricing or input costs.

In the 1989 Berkshire Hathaway shareholders’ letter, Warren Buffett said:

“In a difficult business, […] never is there just one cockroach in the kitchen. The original ‘bargain’ price probably will not turn out to be such a steal after all. Any initial advantage you secure will be quickly eroded by the low return that the business earns.

“For example, if you buy a business for $8 million that can be sold or liquidated for $10 million and promptly take either course, you can realize a high return. But the investment will disappoint if the business is sold for $10 million in ten years and in the interim has annually earned and distributed only a few percent on cost.”

Charlie Munger adds:

"As the old saying goes, there are only two types of investor: those who can’t time the markets, and those who don’t know they can’t time the markets"

“Time is the friend of the wonderful business, the enemy of the mediocre.”

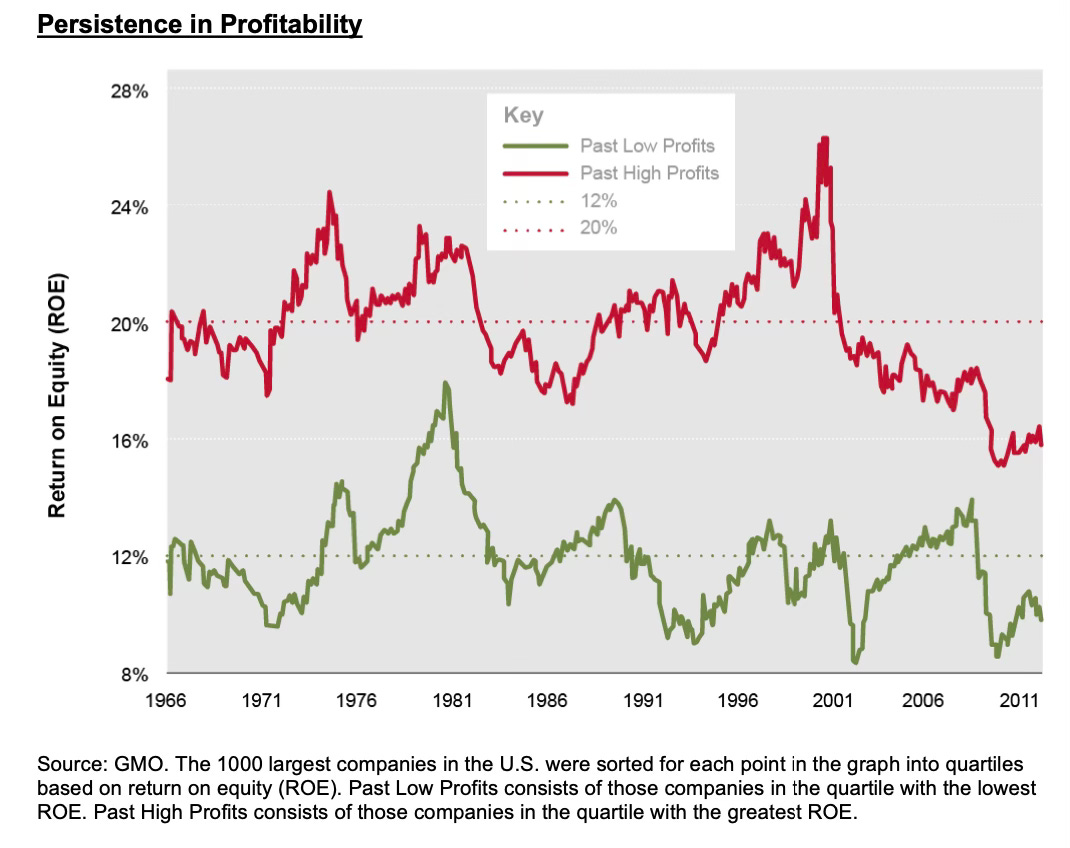

The chart below illustrates that low-quality businesses consistently generate low profitability over time (green line). Energy, utilities, airlines, and discretionary retail companies come to mind. It's just too competitive or too capital-intensive to make it profitable over the cycle.

But it’s never quite simple to separate the good from the bad.

Good companies are not immune to bad periods and are negatively affected by economic downcycles. Their share prices might drop by 40%, often driving people to change their opinion of a business’s quality.

Moreover, on an upcycle, everyone benefits from an economic recovery, disguising the bad companies from the good.

By reading Sleep Well Investments, you are on the right track to learn how to select good ones, and I hope you have found a few from our list.

We have recommended 15 high-quality businesses. Their stats exude quality:

average ROIC is 17%, most with a long reinvestment runway.

average free cash flow per share growth is 21% in the past three years, and

average total share return has been 33% per year since IPO.

Why do we own high-quality companies?

It’s the comfort of knowing they can create value over time as they consistently generate ROIC higher than their WACC (cost of capital). Effective reinvestment allows these businesses to weather downturns, overcome competitive pressure, and thus help you to sleep well.

So, the lesson here is that if you can’t time the market (or know you can’t) and are a long-term investor, choose quality over value.

3. Return on invested capital is a better value creation metric than earning per share.

The third lesson I learned from Terry Smith is that earnings per share (EPS) is often mistaken for value creation. He argues it can be ‘sugar coated’ with acquisitions, cost-cutting, and share buybacks.

While these are all legitimate ways of improving EPS and making a company's fundamentals look good, there are only so many costs and shares you can cut and buy back, and value creation through acquisitions requires a disciplined and decentralized capital allocation process that only a few can execute.

As a result, Terry Smith prefers focusing on high ROIC businesses. Why?

Companies that can consistently generate higher returns than their cost of capital have no limit to the value they can create. This means they can compound their earnings until the reinvestment opportunity dries up.

Sleep Well Investments have a few of them.

Fortinet [deep dive part 1, part 2] and Wisetech have only 4% of the market share [deep dive part 1, part 2], Kinsale has just 2% [deep dive], and MIPS has a new market larger than the existing one to implement its brain protection technology [deep dive]. Meanwhile, Sea Limited’s markets still have over 300M people who have not used its e-commerce and fintech products [deep dive].

So, the key takeaway is that ROIC should be used instead of EPS to identify a high-quality business. A company can destroy shareholder value even if it consistently increases its EPS, which brings us to the fourth lesson.

4. Reinvestment rate > Buyback > Dividends

Similarly, suppose you have found a business that can reinvest effectively. In that case, Terry Smith would prefer that the company continue allocating its excess cash to reinvestment (organically > inorganically) rather than buying back shares and paying dividends.

Constellation Software (CSU) and Berkshire Hathaway (BRK.A, BRK. B) are prime examples. They’ve never paid dividends because Mark Leonard and Warren Buffett knew they could reinvest earnings at a higher return.

If they do pay a dividend, investors will have a less-than-optimum outcome as they would have to pay taxes on the dividend and then use that dividend to reinvest it elsewhere, incurring further transaction costs. Hence, it’s better to let both companies reinvest all their excess cash in the first place.

This is also why investing in stocks is better than investing in bonds, which return a fixed amount of earnings each year, and real estate, which pays you fixed rents and cannot reinvest in the property as a company can.

Walk with me over this example:

Three companies, A, B, and C, generated $100 profit in year 0. The following ten years:

Company A reinvests 50% of the $100 earnings at a 20% return rate.

Company B doesn’t reinvest.

Company C reinvests 50% of the $100 earnings at a -10% loss rate.

The result is Company A was able to generate an annual profit of £259/year by year 10, while Company B's earnings power remains at £100/year, and Company C manages only £60/year. In other words:

Company A created more value by compounding its earnings.

Company B stood still like a bond investor receiving a bond coupon.

Company C destroyed value by reinvesting in loss-making projects.

Hence, the ability to effectively reinvest back into the business is a big reason why stocks can compound over time and why some companies create more value than others.

Of course, picking winners is tough. Only 4% of global stocks (2,200 companies out of 55,000) create most of the wealth in the stock market. And high ROIC industries attract competition, which erodes ROIC over time. So, you must be highly selective and know which company is best positioned to defend its ability to reinvest at a high rate effectively.

The good news is that the dislocation of value creation creates opportunities for committed investors. Reading my blog helps 🎯.

To give you a head start, here is a list of 15 sleep-well businesses I have deep-dived into. You will find 90% of what you need to know about their business model, competitors, challenges, and how they can reinvest effectively to maintain/grow their market position. All links to writeups are here.

5. You must pay up for quality

The last lesson is the hardest lesson to implement—for me, anyway. It’s paying up for quality. Why is that?

Investing in a quality company requires a longer time horizon, as the company may take years or decades to realize the result of the invested capital. Even so, it may not be, so you need to understand the competitive landscape well. Moreover, you often pay for a high multiple in the first place.

Since starting Sleep Well Investments, I have already made two significant errors. One was not buying Wisetech [deep dive, update] in January at $70/share because it was trading at 60x FCF; now it’s $125/share. The other was selling VAT Group [deep dive] at $370/share last year for a quick 70% return; now it’s $450/share.

The following takeaway from BCG and Morgan Stanley research brings it home.

Valuation matters much less over time, 5% to be precise. In contrast, sales, profit, and free cash flow contribute 95% of the stock's performance over the ten years.

Charlie Munger put it nicely.

“Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6% return—even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive-looking price, you’ll end up with a fine result.”

Fortunately, I have made eight good purchases (see below) so far, but I don’t want to miss out on outstanding businesses because they appeared expensive in the first year of ownership.

Below is the current ownership of the Sleep Well Portfolio [update monthly]. I look forward to adding more outstanding businesses in the future.

Terry Smith taught me a lot more, and you can learn from him for free below.

Thank you for reading. If you have found my content value-added, subscribe and spread the word so more long-term investors can sleep well.

Reminder: How can Sleep Well Investments help?

High success rate stock picks—33% money-weighted gain per pick since Oct 2023 (76% time-weighted).

Deep research of high-quality businesses and regular tracking. Buy and verify.

Free samples of deep dives, tracking updates, and buy alerts.

Free articles on investment framework to help find quality companies and execute with discipline.

Promote yourself to 6000+ stock market investors (47% open rate) — Contact me: trung.nguyen@sleepwellinvestments.com

I fully agree with all 5 lessons. Easy to say, more difficult to do.

If you want to add a number 6, it is that the person running the business is often more important than the business itself. To understand this better, see: https://rockandturner.substack.com/p/phil-carret-learn-from-the-best