Sea Limited and Mercado Libre Q1'26: Reinvestment Justified? A Zero Sum Game in Brazil?

Market evaluates these businesses by the quarter, I see a differentiated market entry and early outcome. But can both co-exist profitably?

Sleep Well Portfolio consists of time-tested leaders. We screen them using a rigorous checklist and track their theses regularly to determine when to buy. We document all mistakes and successes to help you improve your portfolio. All about us here.

Sea Limited (SE) and Mercado Libre (MELI) have approached my 6 years of ownership. In this period, I have experienced two major stock declines. While the first was broad-based due to the post-COVID hangover, the second and current one is more driven by a new, elevated reinvestment cycle as both lock horns in Brazil. The two positions constitute over 50% of my net worth, so I write from a very biased but very critical and long-term point of view. Past reports below if you want fuller coverage:

SWI’s SE coverage: [deep dive, 4th buy, 3rd buy, 2nd buy, 1st buy, AI risks, Sum-of-parts Valuation, tariff review, Q4'25, Q3’25, Q2’25, Q1’25, Q4’24, Q3’24, Q2’24]

Meli: CEO transition, AI risks, Q3’25, Q2’25, Q1’25, The Most Sleep Well Investment Of LATAM, Top pick for 2025, Q4’24, Q3’24, and Buy Alert.

In this article, I evaluate their investment decisions to determine whether they are justified and whether the Latin American e-commerce sector market is a zero-sum game.

I’ll start with Sea Limited (SE), going in-depth, then Mercado Libre (MELI).

Sea Limited (Decentralized and capital-light logistics investments, 2% ad take rate, 3% penetrated VIP program, Monee, Garena, Investments to counter TikTok Shop)

Mercado Libre (Cross-border and verticalization investments, Margin compression, Long-term impact, Battles against Shopee)

If you are new to SWI, check out our FAQ and Owner Manual.

If you are already an annual member, you can access the Sleep Well Portfolio and Thesis Tracker via the link below.

Our most recent picks and buys are already up by 35%, and all buys since January are back in the green. Patience and discipline are finally showing results.

TLDR (too long didn’t read):

Sea is the largest e-commerce company with ~53% market share and the largest digital-only bank in Southeast Asia. Meli is the largest e-commerce company with >35% market share and >50% in retail digital media, and a top 10 digital bank in Latin America.

Both are clearly dominating their respective markets, born of building the largest distribution moat (the most users and traffic). The next leg of growth can be simplified to:

One, acquiring new users (buyers and merchants), and two, enticing existing ones to spend more, focusing on retention and operational depth.

In my view, acquiring new users from such a dominant position is harder and less productive than the second option. The emergence of TikTok Shop, Temu, and other cross-border platforms also forced Sea and Meli to double down on reinvestment, playing both defense and offense.

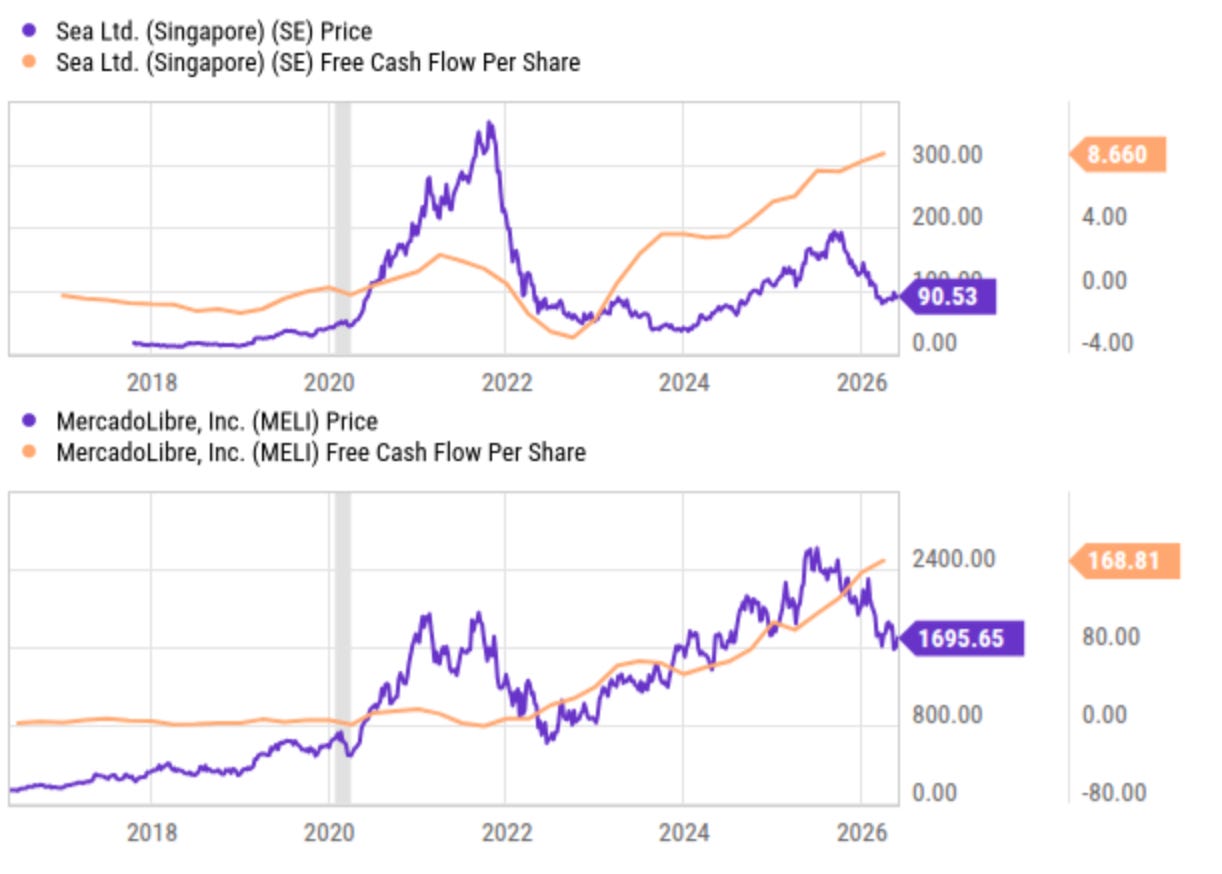

I believe both are reinvesting in the right tools (moving up to higher-value SKUs, building cross-border trade, improving service through in-house logistics and fulfillment, focusing on retention through VIP programs, and integrating financial services), tools that TikTok Shop can’t easily replicate. Early results are strong, and I am confident that both businesses’ free cash flow per share (the ultimate financial metric) will be higher than it is today. And as free cash flow per share diverges from the stock price (see the orange lines below), I will continue to accumulate shares.

Sea Limited

Between May 2022 and Aug 2024, Sea Limited traded around $75/share, with a market cap of $40B.

At the time, the market viewed the company as a grow-at-all-costs business, underpinned by subsidies, marketing intensity, and logistics partnerships. It burned $2B/year to support the e-commerce segment, Shopee. All the while, the main source of cash, its gaming segment, Garena, was shrinking rapidly. That narrative was enough for the market to forget that Sea also had a third segment, a very promising ‘digital-only bank’ in Monee, formerly SeaMoney. At this point, in the worst case, I valued Sea at $44B:

Garena at $12B (12x EBITDA, low range of industry 12-20x EBITDA),

Shopee at $25B (2.5x EV/Revenue, lower than peers at 3x), and

SeaMoney (Monee) at $7B (15x EBITDA).

Still, the stock dropped to a record low of ~$40/share, or a ~$30B market cap.

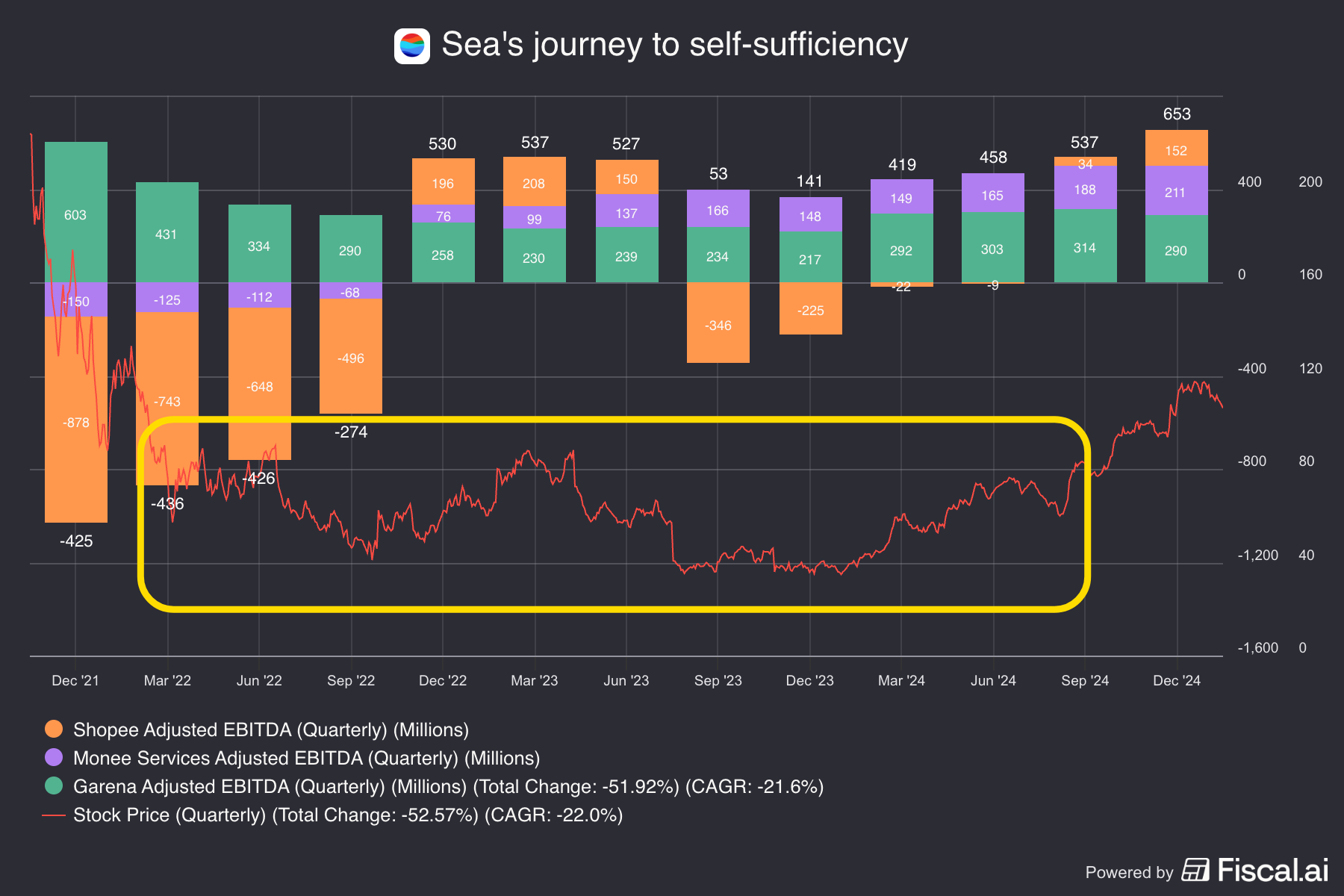

Forrest Li issued a rallying cry in September 2022 to turn the company into a self-sufficient, profitable business. He ruthlessly cut costs, canceled all non-core growth initiatives, and enforced a ‘zero cash compensation’ scheme for executives. It was an all-out change and marked the bottom of Sea’s stock at ~$40/share.

Six quarters later, Shopee reached ‘self-sufficiency’ and was $22M from breakeven. Then, two quarters later, in Q1’25, the company reached the $1B EBITDA mark ($4B annualized).

It was one of the most impressive turnarounds and showed the company can turn the profit tap on and off when required.

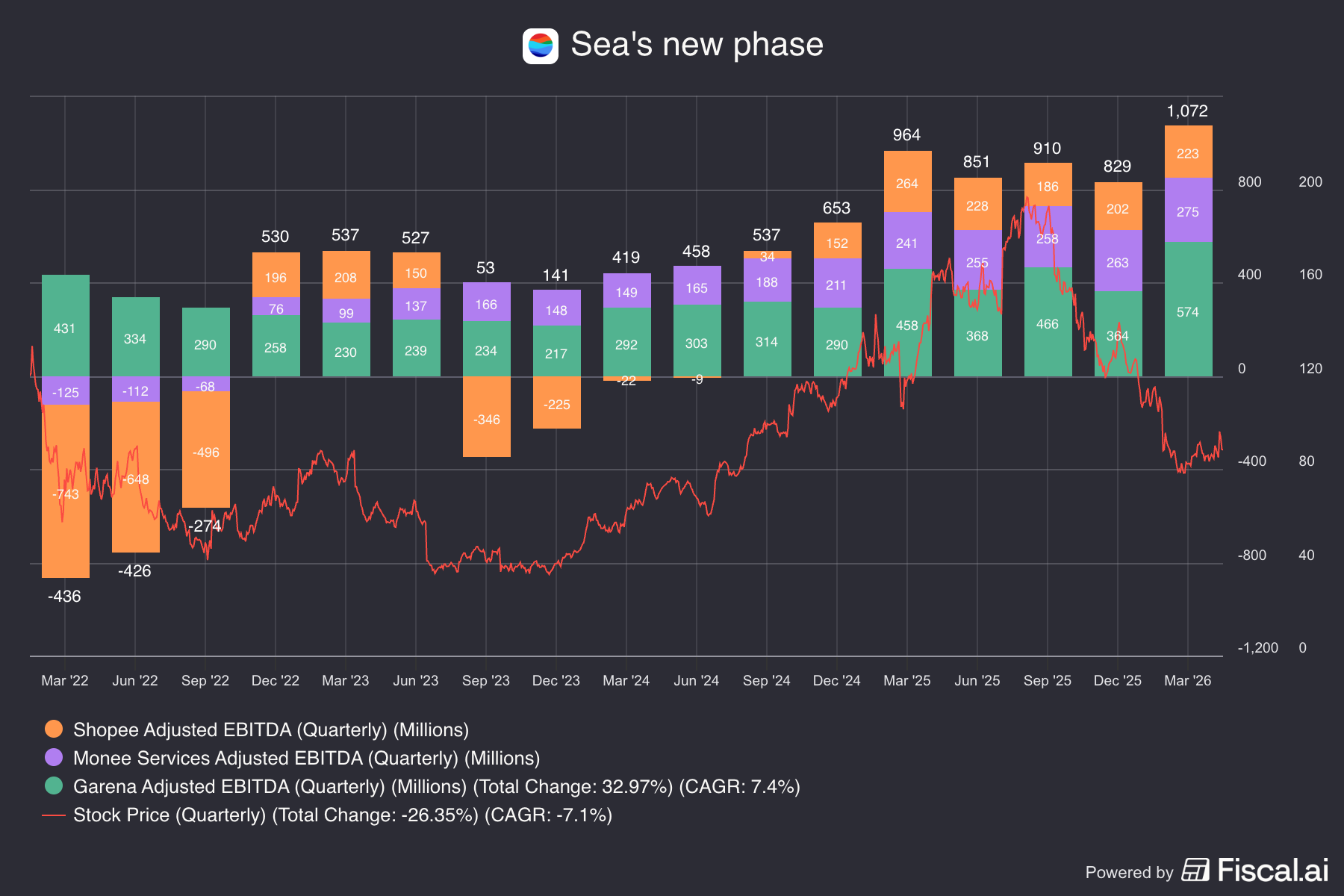

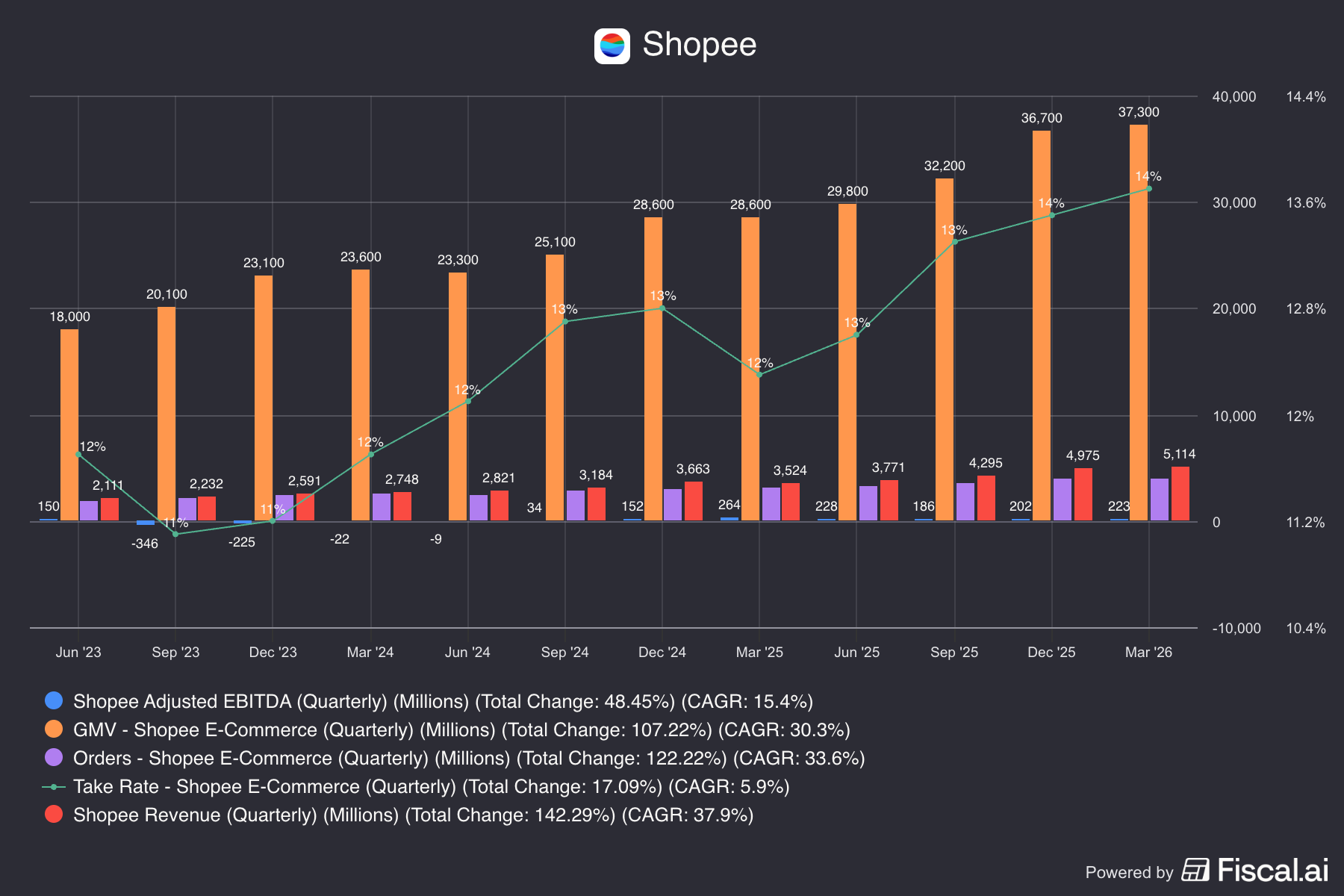

Q1’26 marks 7 quarters of stable profitability. The company also posted:

>$7 billion of revenue, representing 47% year-on-year growth.

Adjusted EBITDA exceeded $1 billion for the first time ($4B annualized)

With a market cap of $53 billion, that’s ~13x Adj.EBITDA for a company that is still growing at least 20% for the next 5 years. This is 2x cheaper than when I first pitched the company in Q1’2024 at ~25x Adj. EBITDA.

The question for me is: Can Sea earn multiple times the $4B in Adj.EBITDA in 2037, when I pass on the portfolio to my daughters? How much does it need to reinvest to exist alongside TikTok Shop and Mercado Libre (in Brazil)?

In other words, I care about Sea’s future earning power in 2037 and beyond. That’s very different from the market’s focus.

Sea’s Q1’26 financial commentary

On Shopee:

Gross merchandise value (GMV) grew 30% YoY and posted a $223M Adj EBITDA.

Compared to Q1’2024, when the share price was about what it is today:

GMV has increased by 60%, to $37B vs $23B

Revenue has increased by 64%, to $5.1B (take rate increased from 12-13%)

Adj. EBITDA has increased to $233M, from breaking even.

Everything has gone in the right direction.

Underneath the numbers is a richer ecosystem of broader SKUs at lower prices, with financing options, faster delivery, and refunds, which broadens to more diverse shoppers and VIP shoppers. AI also continued to accelerate the business

around 80% of customer queries are now handled by our AI chatbot. AI usage helped reduce customer service cost per contact by around 30% year-on-year while maintaining high satisfaction rates — Q1’26

When the ecosystem creates more value, the company can improve monetization.

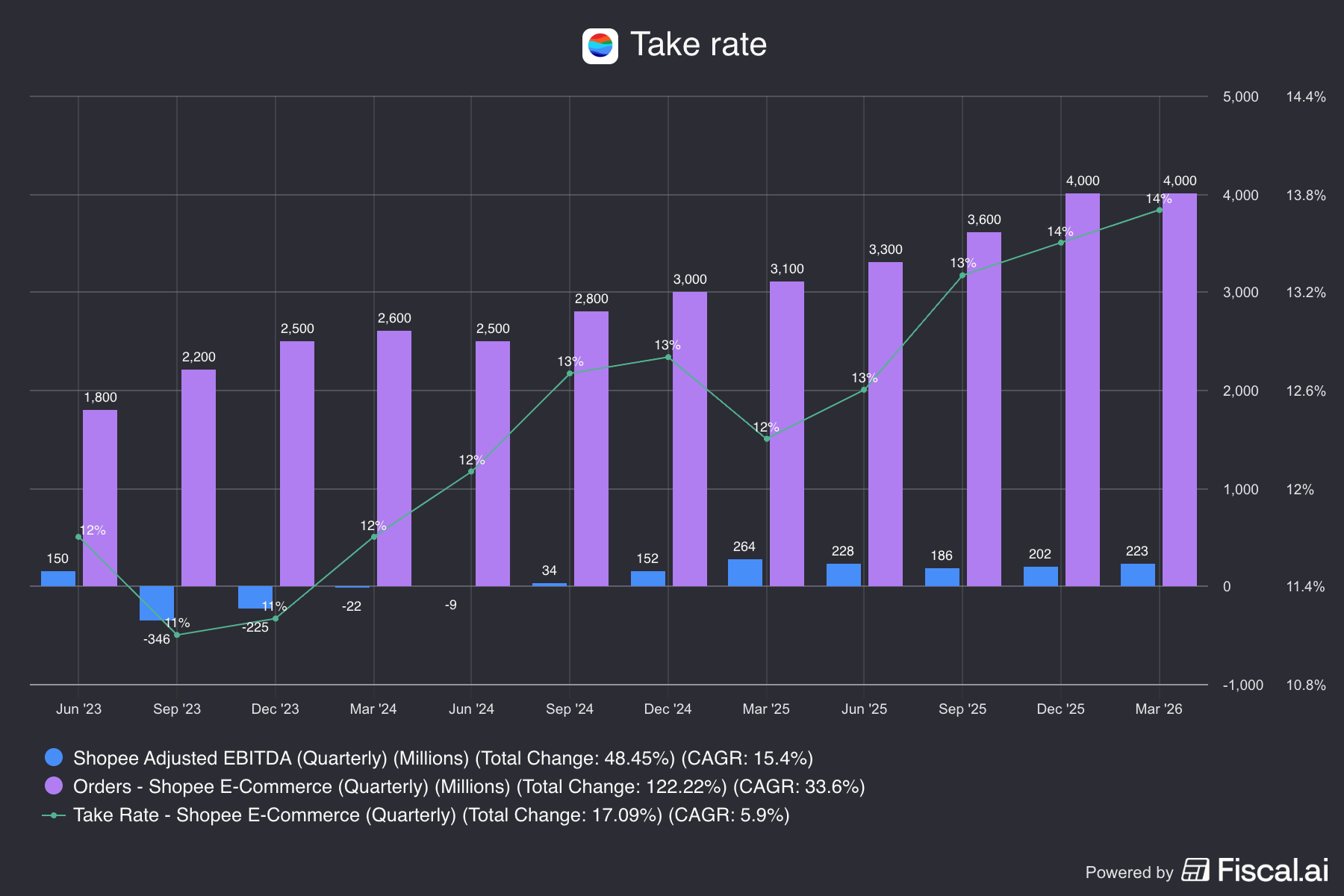

That’s why we saw a gradual increase in take rate to 14% from 12%.

At the center of it is ad revenue, which grew 80%, accelerating the pace of growth since it was first discussed in Q1’24. This is one of the most forward indicators of a marketplace's health. Why? Ads reflect merchants’ intention to invest in their business on Shopee. If they see strong traffic and strong buyer retention, merchants will invest more.

Ad revenue grew 80% and ad take rate increased by more than 90 basis points year-on-year.

Ad-paying sellers and their average ad spend both increased by around 35% year-on-year, reflecting the strong value sellers see in our ad offerings.

Average monthly active buyers increased 16% year-on-year, and the buyer purchase frequency grew around 12% year-on-year.

Looking back at my original thesis and the quarterly commentary summary below, we can see the rapid progression toward a 5-7% ad take rate.